Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeStochastic Volatility Modelling with LSTM Networks: A Hybrid Approach for S&P 500 Index Volatility Forecasting

Dec 13, 2025Accurate volatility forecasting is essential in banking, investment, and risk management, because expectations about future market movements directly influence current decisions. This study proposes a hybrid modelling framework that integrates a Stochastic Volatility model with a Long Short Term Memory neural network. The SV model improves statistical precision and captures latent volatility dynamics, especially in response to unforeseen events, while the LSTM network enhances the model's ability to detect complex nonlinear patterns in financial time series. The forecasting is conducted using daily data from the S and P 500 index, covering the period from January 1 1998 to December 31 2024. A rolling window approach is employed to train the model and generate one step ahead volatility forecasts. The performance of the hybrid SV-LSTM model is evaluated through both statistical testing and investment simulations. The results show that the hybrid approach outperforms both the standalone SV and LSTM models and contributes to the development of volatility modelling techniques, providing a foundation for improving risk assessment and strategic investment planning in the context of the S and P 500.

Alternative Loss Function in Evaluation of Transformer Models

Jul 24, 2025The proper design and architecture of testing machine learning models, especially in their application to quantitative finance problems, is crucial. The most important aspect of this process is selecting an adequate loss function for training, validation, estimation purposes, and hyperparameter tuning. Therefore, in this research, through empirical experiments on equity and cryptocurrency assets, we apply the Mean Absolute Directional Loss (MADL) function, which is more adequate for optimizing forecast-generating models used in algorithmic investment strategies. The MADL function results are compared between Transformer and LSTM models, and we show that in almost every case, Transformer results are significantly better than those obtained with LSTM.

Enhancing literature review with LLM and NLP methods. Algorithmic trading case

Oct 23, 2024This study utilizes machine learning algorithms to analyze and organize knowledge in the field of algorithmic trading. By filtering a dataset of 136 million research papers, we identified 14,342 relevant articles published between 1956 and Q1 2020. We compare traditional practices-such as keyword-based algorithms and embedding techniques-with state-of-the-art topic modeling methods that employ dimensionality reduction and clustering. This comparison allows us to assess the popularity and evolution of different approaches and themes within algorithmic trading. We demonstrate the usefulness of Natural Language Processing (NLP) in the automatic extraction of knowledge, highlighting the new possibilities created by the latest iterations of Large Language Models (LLMs) like ChatGPT. The rationale for focusing on this topic stems from our analysis, which reveals that research articles on algorithmic trading are increasing at a faster rate than the overall number of publications. While stocks and main indices comprise more than half of all assets considered, certain asset classes, such as cryptocurrencies, exhibit a much stronger growth trend. Machine learning models have become the most popular methods in recent years. The study demonstrates the efficacy of LLMs in refining datasets and addressing intricate questions about the analyzed articles, such as comparing the efficiency of different models. Our research shows that by decomposing tasks into smaller components and incorporating reasoning steps, we can effectively tackle complex questions supported by case analyses. This approach contributes to a deeper understanding of algorithmic trading methodologies and underscores the potential of advanced NLP techniques in literature reviews.

The Hybrid Forecast of S&P 500 Volatility ensembled from VIX, GARCH and LSTM models

Jul 23, 2024Predicting the S&P 500 index volatility is crucial for investors and financial analysts as it helps assess market risk and make informed investment decisions. Volatility represents the level of uncertainty or risk related to the size of changes in a security's value, making it an essential indicator for financial planning. This study explores four methods to improve the accuracy of volatility forecasts for the S&P 500: the established GARCH model, known for capturing historical volatility patterns; an LSTM network that utilizes past volatility and log returns; a hybrid LSTM-GARCH model that combines the strengths of both approaches; and an advanced version of the hybrid model that also factors in the VIX index to gauge market sentiment. This analysis is based on a daily dataset that includes S&P 500 and VIX index data, covering the period from January 3, 2000, to December 21, 2023. Through rigorous testing and comparison, we found that machine learning approaches, particularly the hybrid LSTM models, significantly outperform the traditional GARCH model. Including the VIX index in the hybrid model further enhances its forecasting ability by incorporating real-time market sentiment. The results of this study offer valuable insights for achieving more accurate volatility predictions, enabling better risk management and strategic investment decisions in the volatile environment of the S&P 500.

Improving Realized LGD Approximation: A Novel Framework with XGBoost for Handling Missing Cash-Flow Data

Jun 25, 2024

The scope for the accurate calculation of the Loss Given Default (LGD) parameter is comprehensive in terms of financial data. In this research, we aim to explore methods for improving the approximation of realized LGD in conditions of limited access to the cash-flow data. We enhance the performance of the method which relies on the differences between exposure values (delta outstanding approach) by employing machine learning (ML) techniques. The research utilizes the data from the mortgage portfolio of one of the European countries and assumes a close resemblance to similar economic contexts. It incorporates non-financial variables and macroeconomic data related to the housing market, improving the accuracy of loss severity approximation. The proposed methodology attempts to mitigate the country-specific (related to the local legal) or portfolio-specific factors in aim to show the general advantage of applying ML techniques, rather than case-specific relation. We developed an XGBoost model that does not rely on cash-flow data yet enhances the accuracy of realized LGD estimation compared to results obtained with the delta outstanding approach. A novel aspect of our work is the detailed exploration of the delta outstanding approach and the methodology for addressing conditions of limited access to cash-flow data through machine learning models.

Statistical arbitrage in multi-pair trading strategy based on graph clustering algorithms in US equities market

Jun 15, 2024

The study seeks to develop an effective strategy based on the novel framework of statistical arbitrage based on graph clustering algorithms. Amalgamation of quantitative and machine learning methods, including the Kelly criterion, and an ensemble of machine learning classifiers have been used to improve risk-adjusted returns and increase immunity to transaction costs over existing approaches. The study seeks to provide an integrated approach to optimal signal detection and risk management. As a part of this approach, innovative ways of optimizing take profit and stop loss functions for daily frequency trading strategies have been proposed and tested. All of the tested approaches outperformed appropriate benchmarks. The best combinations of the techniques and parameters demonstrated significantly better performance metrics than the relevant benchmarks. The results have been obtained under the assumption of realistic transaction costs, but are sensitive to changes in some key parameters.

Hedging Properties of Algorithmic Investment Strategies using Long Short-Term Memory and Time Series models for Equity Indices

Sep 27, 2023

This paper proposes a novel approach to hedging portfolios of risky assets when financial markets are affected by financial turmoils. We introduce a completely novel approach to diversification activity not on the level of single assets but on the level of ensemble algorithmic investment strategies (AIS) built based on the prices of these assets. We employ four types of diverse theoretical models (LSTM - Long Short-Term Memory, ARIMA-GARCH - Autoregressive Integrated Moving Average - Generalized Autoregressive Conditional Heteroskedasticity, momentum, and contrarian) to generate price forecasts, which are then used to produce investment signals in single and complex AIS. In such a way, we are able to verify the diversification potential of different types of investment strategies consisting of various assets (energy commodities, precious metals, cryptocurrencies, or soft commodities) in hedging ensemble AIS built for equity indices (S&P 500 index). Empirical data used in this study cover the period between 2004 and 2022. Our main conclusion is that LSTM-based strategies outperform the other models and that the best diversifier for the AIS built for the S&P 500 index is the AIS built for Bitcoin. Finally, we test the LSTM model for a higher frequency of data (1 hour). We conclude that it outperforms the results obtained using daily data.

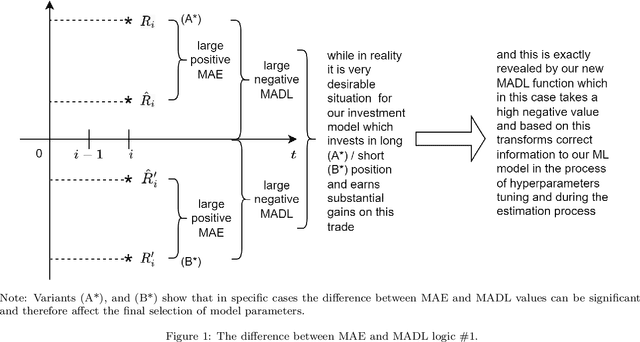

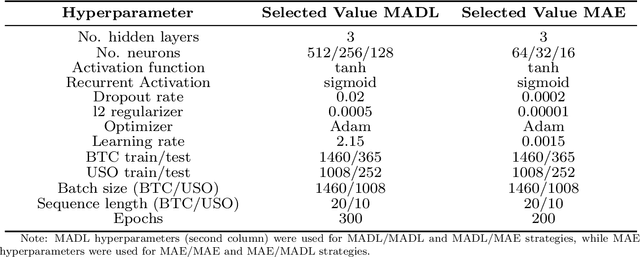

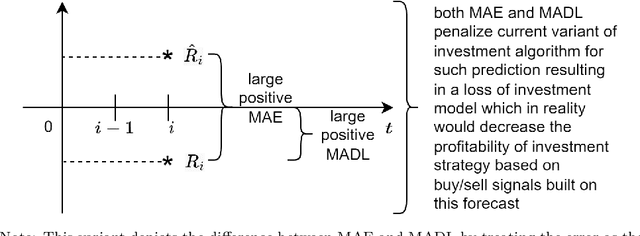

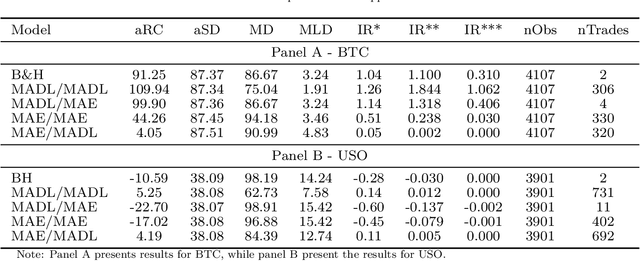

Mean Absolute Directional Loss as a New Loss Function for Machine Learning Problems in Algorithmic Investment Strategies

Sep 19, 2023

This paper investigates the issue of an adequate loss function in the optimization of machine learning models used in the forecasting of financial time series for the purpose of algorithmic investment strategies (AIS) construction. We propose the Mean Absolute Directional Loss (MADL) function, solving important problems of classical forecast error functions in extracting information from forecasts to create efficient buy/sell signals in algorithmic investment strategies. Finally, based on the data from two different asset classes (cryptocurrencies: Bitcoin and commodities: Crude Oil), we show that the new loss function enables us to select better hyperparameters for the LSTM model and obtain more efficient investment strategies, with regard to risk-adjusted return metrics on the out-of-sample data.