Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeAlternative Loss Function in Evaluation of Transformer Models

Jul 24, 2025

The proper design and architecture of testing machine learning models, especially in their application to quantitative finance problems, is crucial. The most important aspect of this process is selecting an adequate loss function for training, validation, estimation purposes, and hyperparameter tuning. Therefore, in this research, through empirical experiments on equity and cryptocurrency assets, we apply the Mean Absolute Directional Loss (MADL) function, which is more adequate for optimizing forecast-generating models used in algorithmic investment strategies. The MADL function results are compared between Transformer and LSTM models, and we show that in almost every case, Transformer results are significantly better than those obtained with LSTM.

Can Artificial Intelligence Trade the Stock Market?

Jun 05, 2025The paper explores the use of Deep Reinforcement Learning (DRL) in stock market trading, focusing on two algorithms: Double Deep Q-Network (DDQN) and Proximal Policy Optimization (PPO) and compares them with Buy and Hold benchmark. It evaluates these algorithms across three currency pairs, the S&P 500 index and Bitcoin, on the daily data in the period of 2019-2023. The results demonstrate DRL's effectiveness in trading and its ability to manage risk by strategically avoiding trades in unfavorable conditions, providing a substantial edge over classical approaches, based on supervised learning in terms of risk-adjusted returns.

Hedging Properties of Algorithmic Investment Strategies using Long Short-Term Memory and Time Series models for Equity Indices

Sep 27, 2023

This paper proposes a novel approach to hedging portfolios of risky assets when financial markets are affected by financial turmoils. We introduce a completely novel approach to diversification activity not on the level of single assets but on the level of ensemble algorithmic investment strategies (AIS) built based on the prices of these assets. We employ four types of diverse theoretical models (LSTM - Long Short-Term Memory, ARIMA-GARCH - Autoregressive Integrated Moving Average - Generalized Autoregressive Conditional Heteroskedasticity, momentum, and contrarian) to generate price forecasts, which are then used to produce investment signals in single and complex AIS. In such a way, we are able to verify the diversification potential of different types of investment strategies consisting of various assets (energy commodities, precious metals, cryptocurrencies, or soft commodities) in hedging ensemble AIS built for equity indices (S&P 500 index). Empirical data used in this study cover the period between 2004 and 2022. Our main conclusion is that LSTM-based strategies outperform the other models and that the best diversifier for the AIS built for the S&P 500 index is the AIS built for Bitcoin. Finally, we test the LSTM model for a higher frequency of data (1 hour). We conclude that it outperforms the results obtained using daily data.

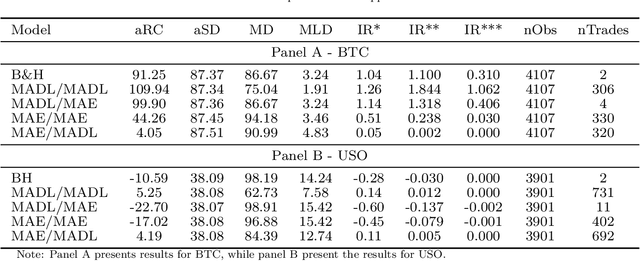

Mean Absolute Directional Loss as a New Loss Function for Machine Learning Problems in Algorithmic Investment Strategies

Sep 19, 2023

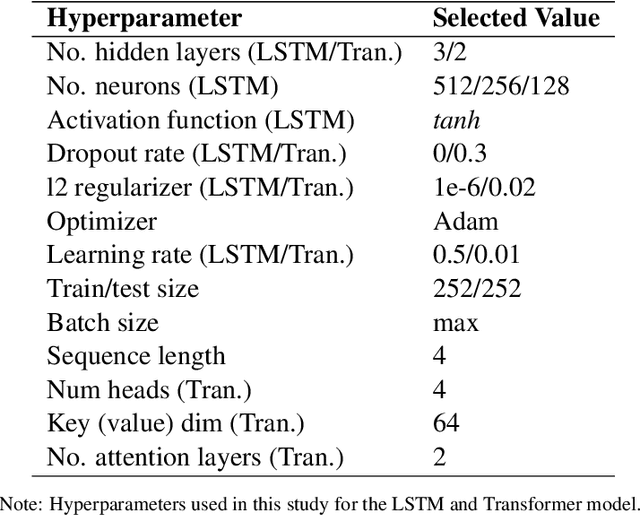

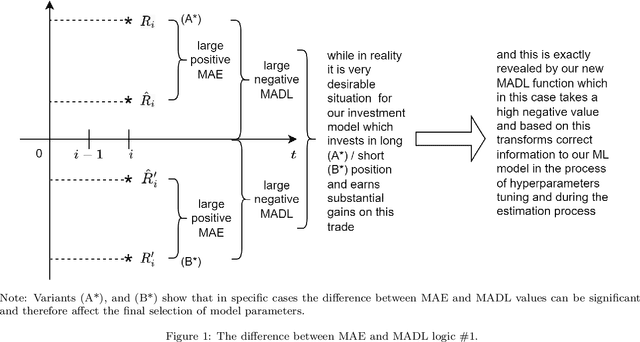

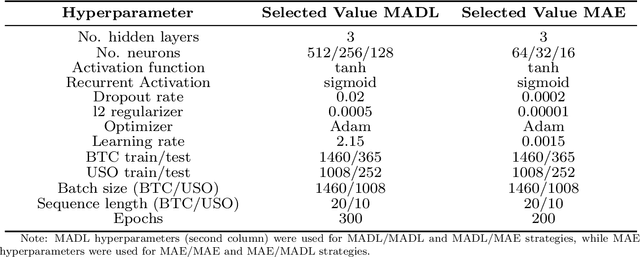

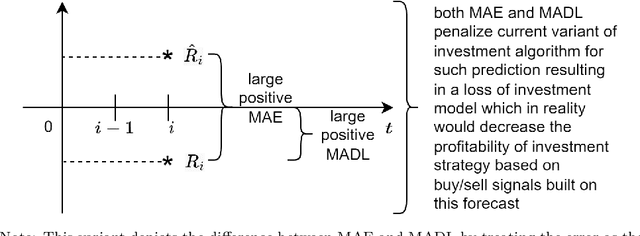

This paper investigates the issue of an adequate loss function in the optimization of machine learning models used in the forecasting of financial time series for the purpose of algorithmic investment strategies (AIS) construction. We propose the Mean Absolute Directional Loss (MADL) function, solving important problems of classical forecast error functions in extracting information from forecasts to create efficient buy/sell signals in algorithmic investment strategies. Finally, based on the data from two different asset classes (cryptocurrencies: Bitcoin and commodities: Crude Oil), we show that the new loss function enables us to select better hyperparameters for the LSTM model and obtain more efficient investment strategies, with regard to risk-adjusted return metrics on the out-of-sample data.