Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeForex trading and Twitter: Spam, bots, and reputation manipulation

Apr 16, 2018

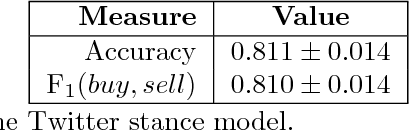

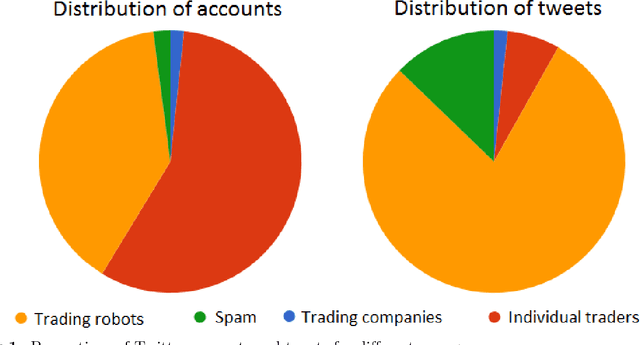

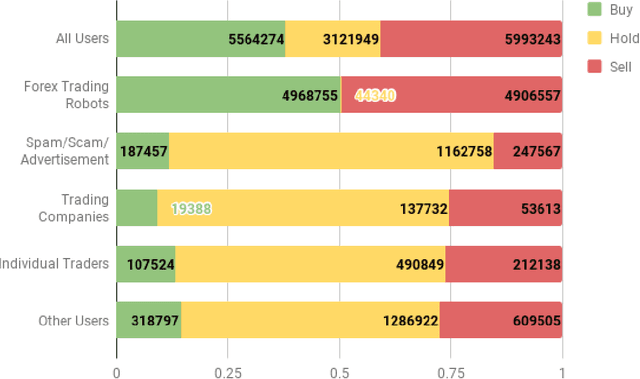

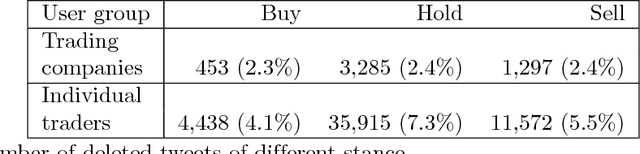

Currency trading (Forex) is the largest world market in terms of volume. We analyze trading and tweeting about the EUR-USD currency pair over a period of three years. First, a large number of tweets were manually labeled, and a Twitter stance classification model is constructed. The model then classifies all the tweets by the trading stance signal: buy, hold, or sell (EUR vs. USD). The Twitter stance is compared to the actual currency rates by applying the event study methodology, well-known in financial economics. It turns out that there are large differences in Twitter stance distribution and potential trading returns between the four groups of Twitter users: trading robots, spammers, trading companies, and individual traders. Additionally, we observe attempts of reputation manipulation by post festum removal of tweets with poor predictions, and deleting/reposting of identical tweets to increase the visibility without tainting one's Twitter timeline.