Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeProbabilistic Multi-Regional Solar Power Forecasting with Any-Quantile Recurrent Neural Networks

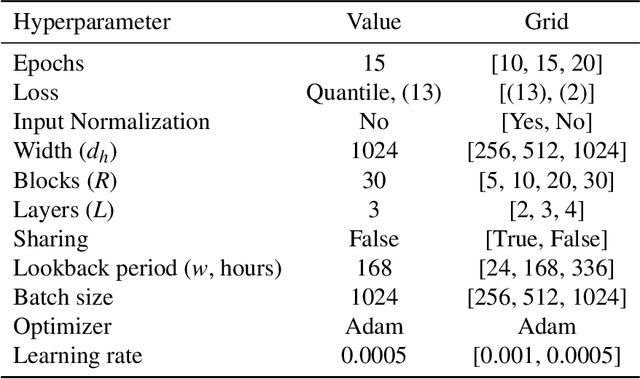

Feb 05, 2026The increasing penetration of photovoltaic (PV) generation introduces significant uncertainty into power system operation, necessitating forecasting approaches that extend beyond deterministic point predictions. This paper proposes an any-quantile probabilistic forecasting framework for multi-regional PV power generation based on the Any-Quantile Recurrent Neural Network (AQ-RNN). The model integrates an any-quantile forecasting paradigm with a dual-track recurrent architecture that jointly processes series-specific and cross-regional contextual information, supported by dilated recurrent cells, patch-based temporal modeling, and a dynamic ensemble mechanism. The proposed framework enables the estimation of calibrated conditional quantiles at arbitrary probability levels within a single trained model and effectively exploits spatial dependencies to enhance robustness at the system level. The approach is evaluated using 30 years of hourly PV generation data from 259 European regions and compared against established statistical and neural probabilistic baselines. The results demonstrate consistent improvements in forecast accuracy, calibration, and prediction interval quality, underscoring the suitability of the proposed method for uncertainty-aware energy management and operational decision-making in renewable-dominated power systems.

Forecasting Cryptocurrency Prices using Contextual ES-adRNN with Exogenous Variables

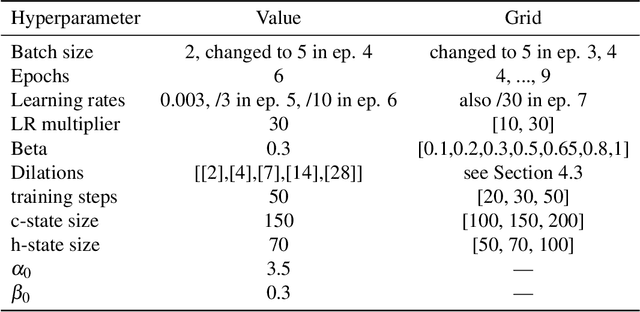

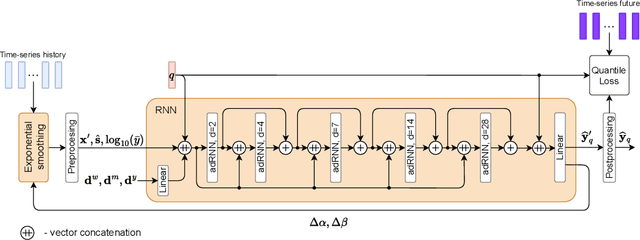

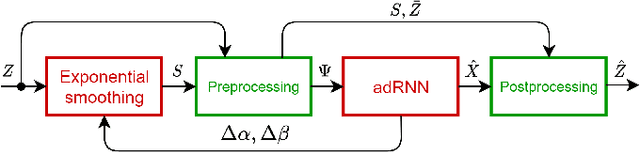

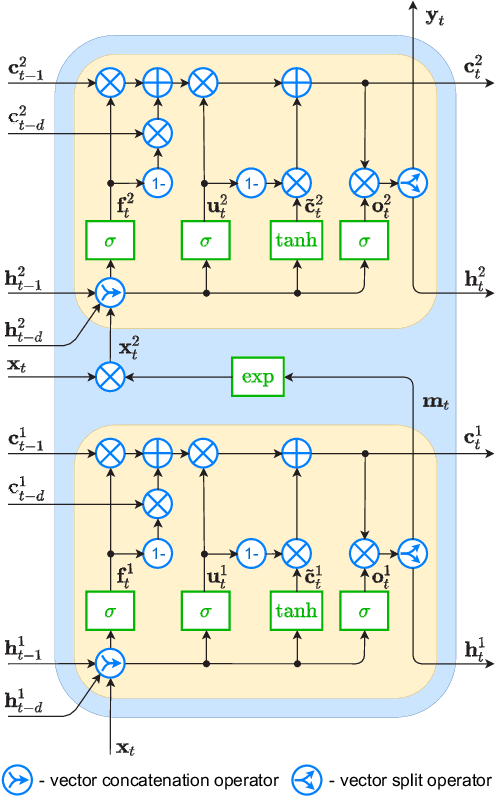

Apr 11, 2025In this paper, we introduce a new approach to multivariate forecasting cryptocurrency prices using a hybrid contextual model combining exponential smoothing (ES) and recurrent neural network (RNN). The model consists of two tracks: the context track and the main track. The context track provides additional information to the main track, extracted from representative series. This information as well as information extracted from exogenous variables is dynamically adjusted to the individual series forecasted by the main track. The RNN stacked architecture with hierarchical dilations, incorporating recently developed attentive dilated recurrent cells, allows the model to capture short and long-term dependencies across time series and dynamically weight input information. The model generates both point daily forecasts and predictive intervals for one-day, one-week and four-week horizons. We apply our model to forecast prices of 15 cryptocurrencies based on 17 input variables and compare its performance with that of comparative models, including both statistical and ML ones.

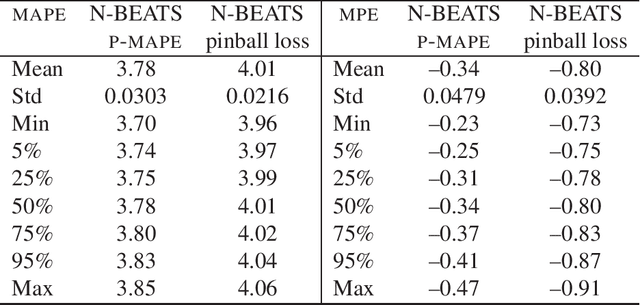

Enhanced N-BEATS for Mid-Term Electricity Demand Forecasting

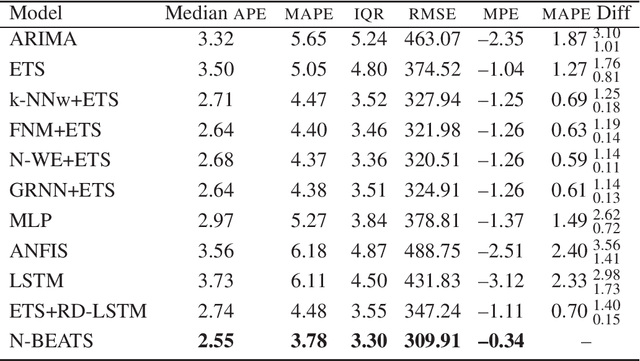

Dec 02, 2024This paper presents an enhanced N-BEATS model, N-BEATS*, for improved mid-term electricity load forecasting (MTLF). Building on the strengths of the original N-BEATS architecture, which excels in handling complex time series data without requiring preprocessing or domain-specific knowledge, N-BEATS* introduces two key modifications. (1) A novel loss function -- combining pinball loss based on MAPE with normalized MSE, the new loss function allows for a more balanced approach by capturing both L1 and L2 loss terms. (2) A modified block architecture -- the internal structure of the N-BEATS blocks is adjusted by introducing a destandardization component to harmonize the processing of different time series, leading to more efficient and less complex forecasting tasks. Evaluated on real-world monthly electricity consumption data from 35 European countries, N-BEATS* demonstrates superior performance compared to its predecessor and other established forecasting methods, including statistical, machine learning, and hybrid models. N-BEATS* achieves the lowest MAPE and RMSE, while also exhibiting the lowest dispersion in forecast errors.

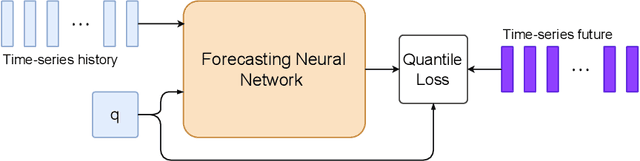

Any-Quantile Probabilistic Forecasting of Short-Term Electricity Demand

Apr 26, 2024

Power systems operate under uncertainty originating from multiple factors that are impossible to account for deterministically. Distributional forecasting is used to control and mitigate risks associated with this uncertainty. Recent progress in deep learning has helped to significantly improve the accuracy of point forecasts, while accurate distributional forecasting still presents a significant challenge. In this paper, we propose a novel general approach for distributional forecasting capable of predicting arbitrary quantiles. We show that our general approach can be seamlessly applied to two distinct neural architectures leading to the state-of-the-art distributional forecasting results in the context of short-term electricity demand forecasting task. We empirically validate our method on 35 hourly electricity demand time-series for European countries. Our code is available here: https://github.com/boreshkinai/any-quantile.

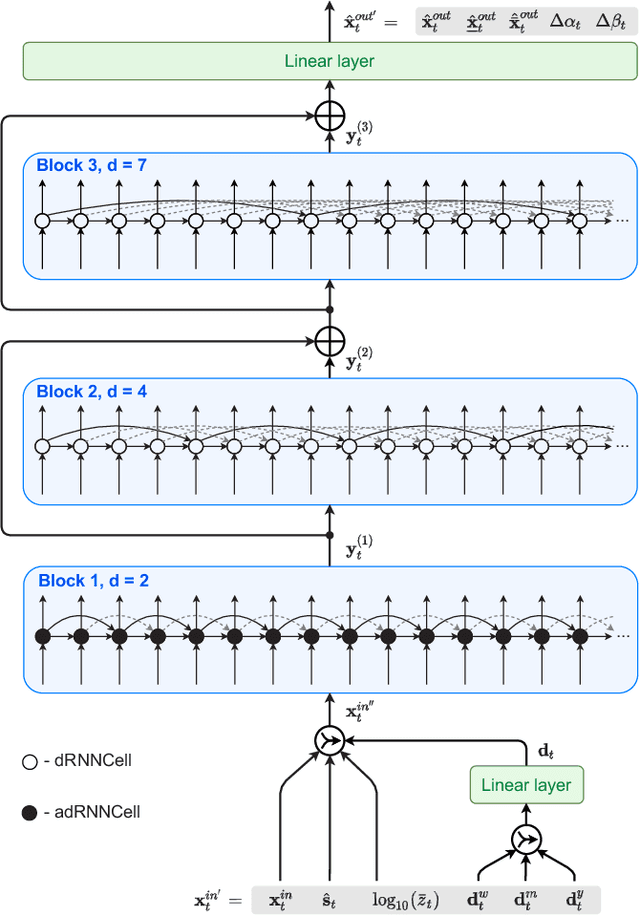

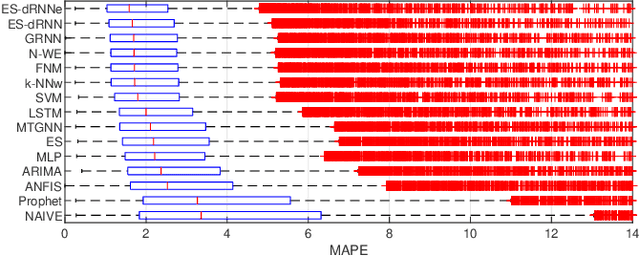

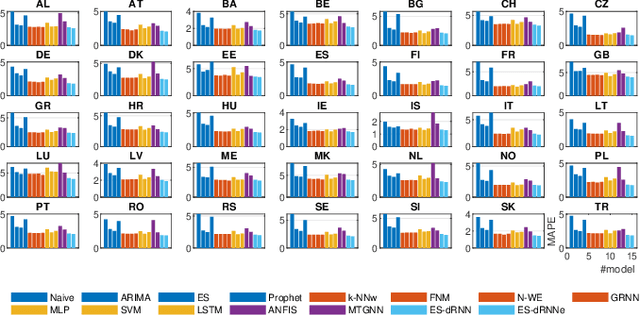

Contextually Enhanced ES-dRNN with Dynamic Attention for Short-Term Load Forecasting

Dec 18, 2022

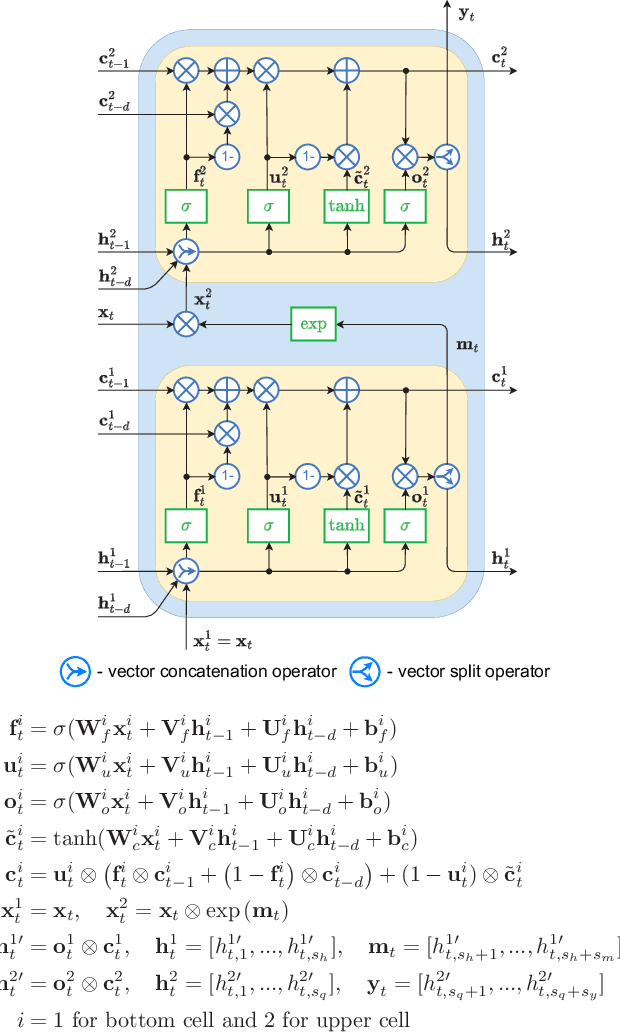

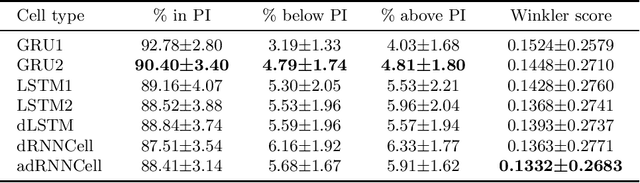

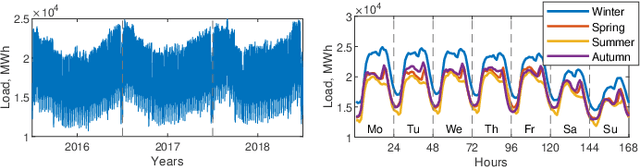

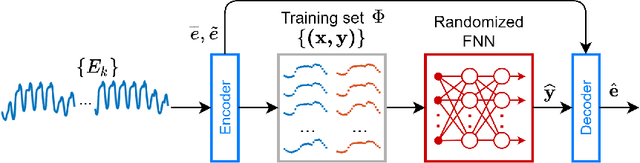

In this paper, we propose a new short-term load forecasting (STLF) model based on contextually enhanced hybrid and hierarchical architecture combining exponential smoothing (ES) and a recurrent neural network (RNN). The model is composed of two simultaneously trained tracks: the context track and the main track. The context track introduces additional information to the main track. It is extracted from representative series and dynamically modulated to adjust to the individual series forecasted by the main track. The RNN architecture consists of multiple recurrent layers stacked with hierarchical dilations and equipped with recently proposed attentive dilated recurrent cells. These cells enable the model to capture short-term, long-term and seasonal dependencies across time series as well as to weight dynamically the input information. The model produces both point forecasts and predictive intervals. The experimental part of the work performed on 35 forecasting problems shows that the proposed model outperforms in terms of accuracy its predecessor as well as standard statistical models and state-of-the-art machine learning models.

Recurrent Neural Networks for Forecasting Time Series with Multiple Seasonality: A Comparative Study

Mar 17, 2022

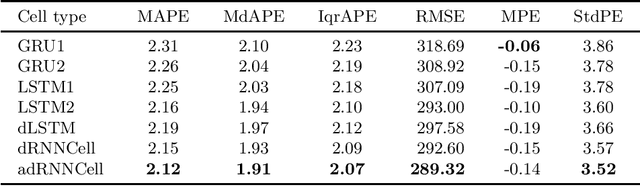

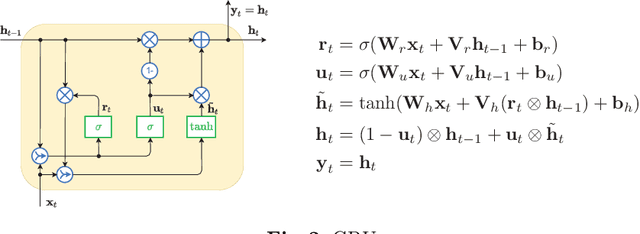

This paper compares recurrent neural networks (RNNs) with different types of gated cells for forecasting time series with multiple seasonality. The cells we compare include classical long short term memory (LSTM), gated recurrent unit (GRU), modified LSTM with dilation, and two new cells we proposed recently, which are equipped with dilation and attention mechanisms. To model the temporal dependencies of different scales, our RNN architecture has multiple dilated recurrent layers stacked with hierarchical dilations. The proposed RNN produces both point forecasts and predictive intervals (PIs) for them. An empirical study concerning short-term electrical load forecasting for 35 European countries confirmed that the new gated cells with dilation and attention performed best.

ES-dRNN with Dynamic Attention for Short-Term Load Forecasting

Mar 02, 2022

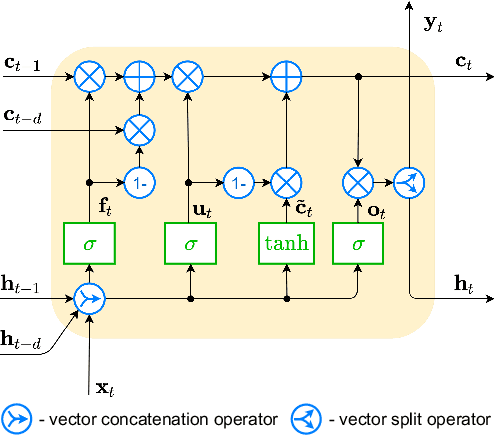

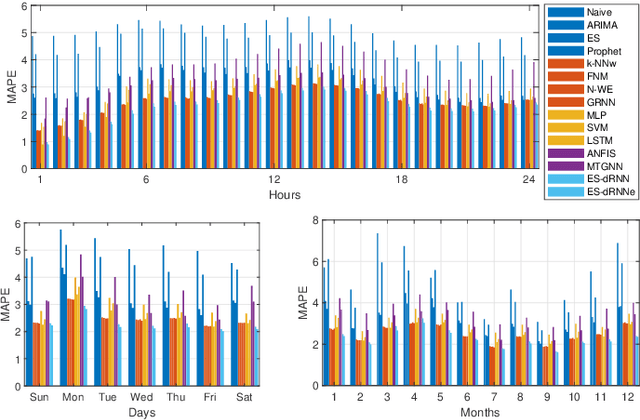

Short-term load forecasting (STLF) is a challenging problem due to the complex nature of the time series expressing multiple seasonality and varying variance. This paper proposes an extension of a hybrid forecasting model combining exponential smoothing and dilated recurrent neural network (ES-dRNN) with a mechanism for dynamic attention. We propose a new gated recurrent cell -- attentive dilated recurrent cell, which implements an attention mechanism for dynamic weighting of input vector components. The most relevant components are assigned greater weights, which are subsequently dynamically fine-tuned. This attention mechanism helps the model to select input information and, along with other mechanisms implemented in ES-dRNN, such as adaptive time series processing, cross-learning, and multiple dilation, leads to a significant improvement in accuracy when compared to well-established statistical and state-of-the-art machine learning forecasting models. This was confirmed in the extensive experimental study concerning STLF for 35 European countries.

ES-dRNN: A Hybrid Exponential Smoothing and Dilated Recurrent Neural Network Model for Short-Term Load Forecasting

Dec 05, 2021

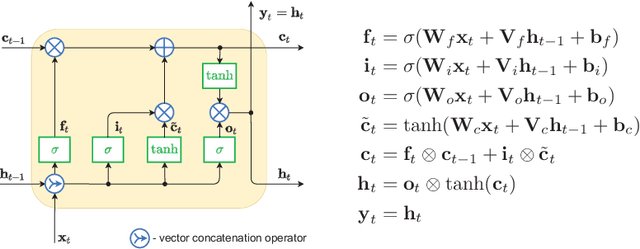

Short-term load forecasting (STLF) is challenging due to complex time series (TS) which express three seasonal patterns and a nonlinear trend. This paper proposes a novel hybrid hierarchical deep learning model that deals with multiple seasonality and produces both point forecasts and predictive intervals (PIs). It combines exponential smoothing (ES) and a recurrent neural network (RNN). ES extracts dynamically the main components of each individual TS and enables on-the-fly deseasonalization, which is particularly useful when operating on a relatively small data set. A multi-layer RNN is equipped with a new type of dilated recurrent cell designed to efficiently model both short and long-term dependencies in TS. To improve the internal TS representation and thus the model's performance, RNN learns simultaneously both the ES parameters and the main mapping function transforming inputs into forecasts. We compare our approach against several baseline methods, including classical statistical methods and machine learning (ML) approaches, on STLF problems for 35 European countries. The empirical study clearly shows that the proposed model has high expressive power to solve nonlinear stochastic forecasting problems with TS including multiple seasonality and significant random fluctuations. In fact, it outperforms both statistical and state-of-the-art ML models in terms of accuracy.

Ensembles of Randomized NNs for Pattern-based Time Series Forecasting

Jul 08, 2021

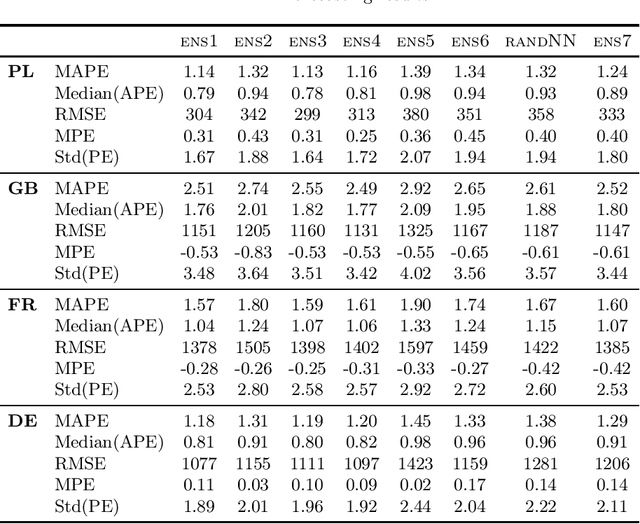

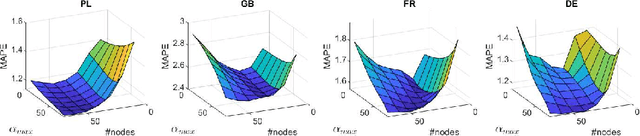

In this work, we propose an ensemble forecasting approach based on randomized neural networks. Improved randomized learning streamlines the fitting abilities of individual learners by generating network parameters in accordance with the data and target function features. A pattern-based representation of time series makes the proposed approach suitable for forecasting time series with multiple seasonality. We propose six strategies for controlling the diversity of ensemble members. Case studies conducted on four real-world forecasting problems verified the effectiveness and superior performance of the proposed ensemble forecasting approach. It outperformed statistical models as well as state-of-the-art machine learning models in terms of forecasting accuracy. The proposed approach has several advantages: fast and easy training, simple architecture, ease of implementation, high accuracy and the ability to deal with nonstationarity and multiple seasonality in time series.

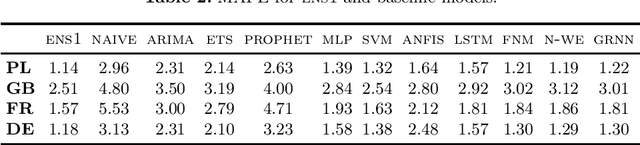

N-BEATS neural network for mid-term electricity load forecasting

Sep 24, 2020

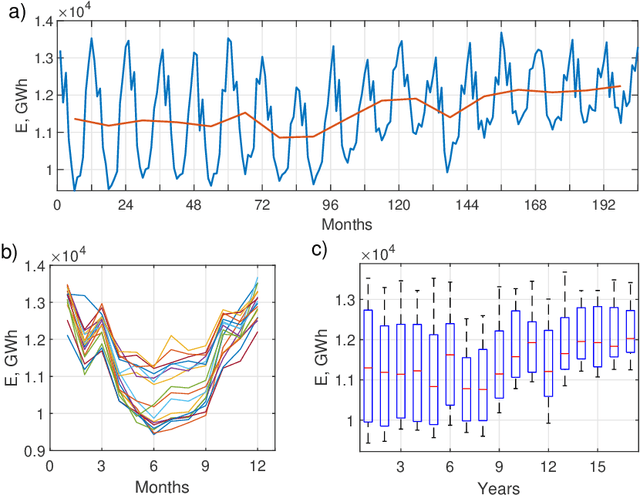

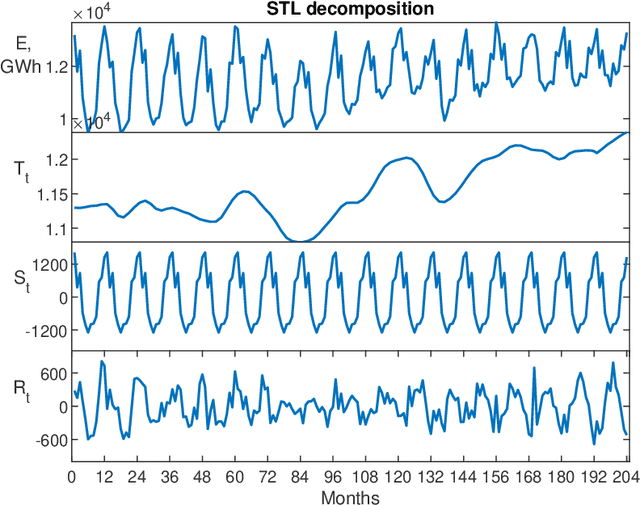

We address the mid-term electricity load forecasting (MTLF) problem. This problem is relevant and challenging. On the one hand, MTLF supports high-level (e.g. country level) decision-making at distant planning horizons (e.g. month, quarter, year). Therefore, financial impact of associated decisions may be significant and it is desirable that they be made based on accurate forecasts. On the other hand, the country level monthly time-series typically associated with MTLF are very complex and stochastic -- including trends, seasonality and significant random fluctuations. In this paper we show that our proposed deep neural network modelling approach based on the N-BEATS neural architecture is very effective at solving MTLF problem. N-BEATS has high expressive power to solve non-linear stochastic forecasting problems. At the same time, it is simple to implement and train, it does not require signal preprocessing. We compare our approach against the set of ten baseline methods, including classical statistical methods, machine learning and hybrid approaches on 35 monthly electricity demand time series for European countries. We show that in terms of the MAPE error metric our method provides statistically significant relative gain of 25% with respect to the classical statistical methods, 28% with respect to classical machine learning methods and 14% with respect to the advanced state-of-the-art hybrid methods combining machine learning and statistical approaches.