Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeSpatial-Temporal Bearing Fault Detection Using Graph Attention Networks and LSTM

Oct 15, 2024

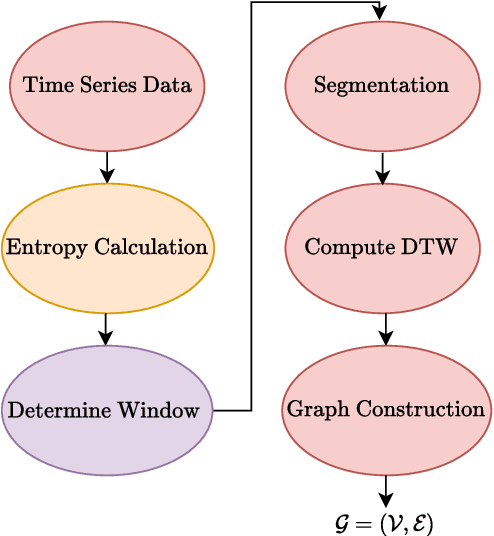

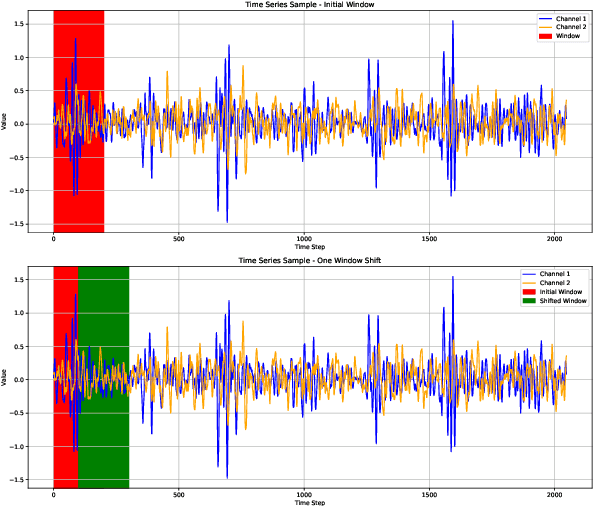

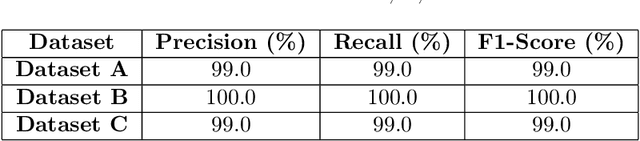

Purpose: This paper aims to enhance bearing fault diagnosis in industrial machinery by introducing a novel method that combines Graph Attention Network (GAT) and Long Short-Term Memory (LSTM) networks. This approach captures both spatial and temporal dependencies within sensor data, improving the accuracy of bearing fault detection under various conditions. Methodology: The proposed method converts time series sensor data into graph representations. GAT captures spatial relationships between components, while LSTM models temporal patterns. The model is validated using the Case Western Reserve University (CWRU) Bearing Dataset, which includes data under different horsepower levels and both normal and faulty conditions. Its performance is compared with methods such as K-Nearest Neighbors (KNN), Local Outlier Factor (LOF), Isolation Forest (IForest) and GNN-based method for bearing fault detection (GNNBFD). Findings: The model achieved outstanding results, with precision, recall, and F1-scores reaching 100\% across various testing conditions. It not only identifies faults accurately but also generalizes effectively across different operational scenarios, outperforming traditional methods. Originality: This research presents a unique combination of GAT and LSTM for fault detection, overcoming the limitations of traditional time series methods by capturing complex spatial-temporal dependencies. Its superior performance demonstrates significant potential for predictive maintenance in industrial applications.

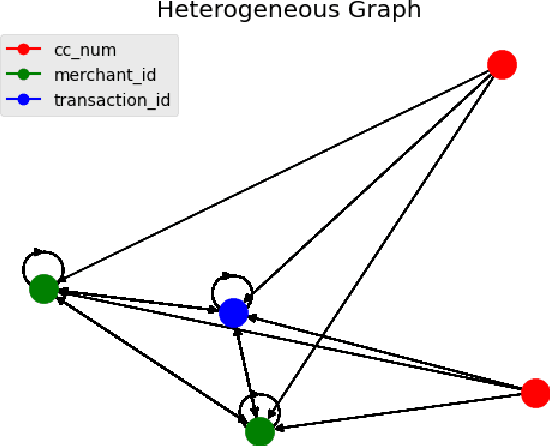

Heterogeneous Graph Auto-Encoder for CreditCard Fraud Detection

Oct 10, 2024

The digital revolution has significantly impacted financial transactions, leading to a notable increase in credit card usage. However, this convenience comes with a trade-off: a substantial rise in fraudulent activities. Traditional machine learning methods for fraud detection often struggle to capture the inherent interconnectedness within financial data. This paper proposes a novel approach for credit card fraud detection that leverages Graph Neural Networks (GNNs) with attention mechanisms applied to heterogeneous graph representations of financial data. Unlike homogeneous graphs, heterogeneous graphs capture intricate relationships between various entities in the financial ecosystem, such as cardholders, merchants, and transactions, providing a richer and more comprehensive data representation for fraud analysis. To address the inherent class imbalance in fraud data, where genuine transactions significantly outnumber fraudulent ones, the proposed approach integrates an autoencoder. This autoencoder, trained on genuine transactions, learns a latent representation and flags deviations during reconstruction as potential fraud. This research investigates two key questions: (1) How effectively can a GNN with an attention mechanism detect and prevent credit card fraud when applied to a heterogeneous graph? (2) How does the efficacy of the autoencoder with attention approach compare to traditional methods? The results are promising, demonstrating that the proposed model outperforms benchmark algorithms such as Graph Sage and FI-GRL, achieving a superior AUC-PR of 0.89 and an F1-score of 0.81. This research significantly advances fraud detection systems and the overall security of financial transactions by leveraging GNNs with attention mechanisms and addressing class imbalance through an autoencoder.