Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeOnline Decision Making for Trading Wind Energy

Sep 05, 2022

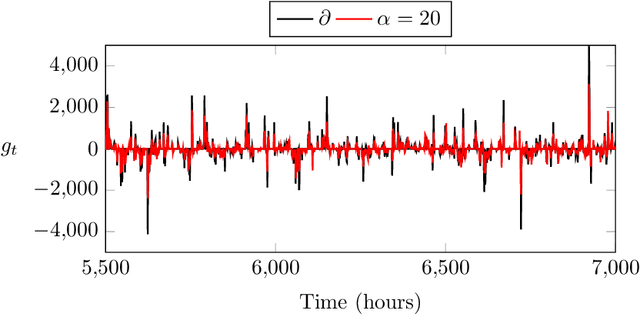

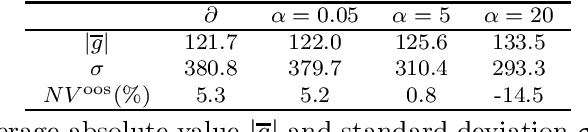

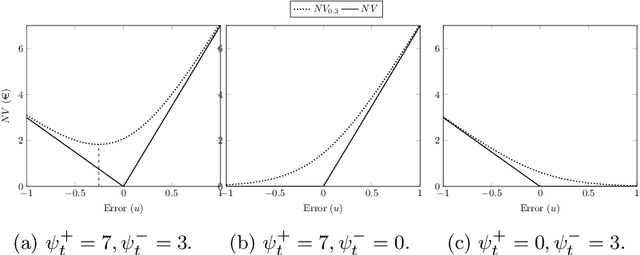

This paper proposes and develops a new algorithm for trading wind energy in electricity markets, within an online learning and optimization framework. In particular, we combine a component-wise adaptive variant of the gradient descent algorithm with recent advances in the feature-driven newsvendor model. This results in an online offering approach capable of leveraging data-rich environments, while adapting to non-stationary characteristics of energy generation and electricity markets, and with a minimal computational burden. The performance of our approach is analyzed based on several numerical experiments, showing both better adaptability to non-stationary uncertain parameters and significant economic gains.

Via