Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeMany learning agents interacting with an agent-based market model

Mar 25, 2023

We consider the dynamics and the interactions of multiple reinforcement learning optimal execution trading agents interacting with a reactive Agent-Based Model (ABM) of a financial market in event time. The model represents a market ecology with 3-trophic levels represented by: optimal execution learning agents, minimally intelligent liquidity takers, and fast electronic liquidity providers. The optimal execution agent classes include buying and selling agents that can either use a combination of limit orders and market orders, or only trade using market orders. The reward function explicitly balances trade execution slippage against the penalty of not executing the order timeously. This work demonstrates how multiple competing learning agents impact a minimally intelligent market simulation as functions of the number of agents, the size of agents' initial orders, and the state spaces used for learning. We use phase space plots to examine the dynamics of the ABM, when various specifications of learning agents are included. Further, we examine whether the inclusion of optimal execution agents that can learn is able to produce dynamics with the same complexity as empirical data. We find that the inclusion of optimal execution agents changes the stylised facts produced by ABM to conform more with empirical data, and are a necessary inclusion for ABMs investigating market micro-structure. However, including execution agents to chartist-fundamentalist-noise ABMs is insufficient to recover the complexity observed in empirical data.

A simple learning agent interacting with an agent-based market model

Aug 22, 2022

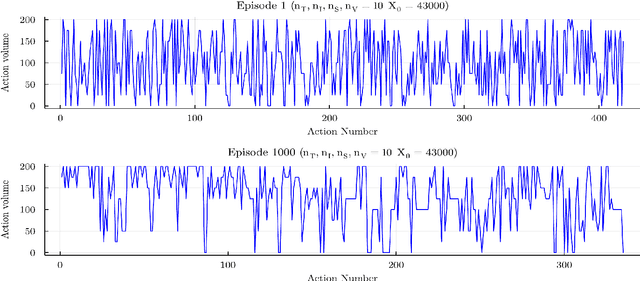

We consider the learning dynamics of a single reinforcement learning optimal execution trading agent when it interacts with an event driven agent-based financial market model. Trading takes place asynchronously through a matching engine in event time. The optimal execution agent is considered at different levels of initial order-sizes and differently sized state spaces. The resulting impact on the agent-based model and market are considered using a calibration approach that explores changes in the empirical stylised facts and price impact curves. Convergence, volume trajectory and action trace plots are used to visualise the learning dynamics. This demonstrates how an optimal execution agent learns optimal trading decisions inside a simulated reactive market framework and how this in turn generates a back-reaction that changes the simulated market through the introduction of strategic order-splitting.