Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeA simple learning agent interacting with an agent-based market model

Paper and Code

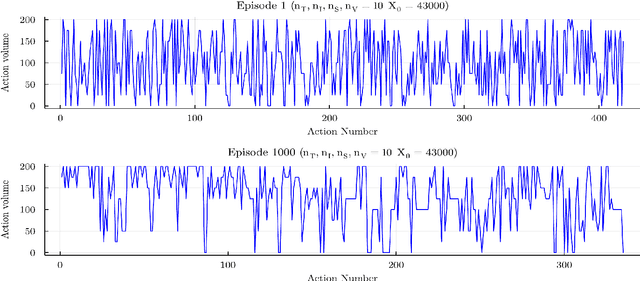

We consider the learning dynamics of a single reinforcement learning optimal execution trading agent when it interacts with an event driven agent-based financial market model. Trading takes place asynchronously through a matching engine in event time. The optimal execution agent is considered at different levels of initial order-sizes and differently sized state spaces. The resulting impact on the agent-based model and market are considered using a calibration approach that explores changes in the empirical stylised facts and price impact curves. Convergence, volume trajectory and action trace plots are used to visualise the learning dynamics. This demonstrates how an optimal execution agent learns optimal trading decisions inside a simulated reactive market framework and how this in turn generates a back-reaction that changes the simulated market through the introduction of strategic order-splitting.