Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeTSEC: a framework for online experimentation under experimental constraints

Jan 17, 2021

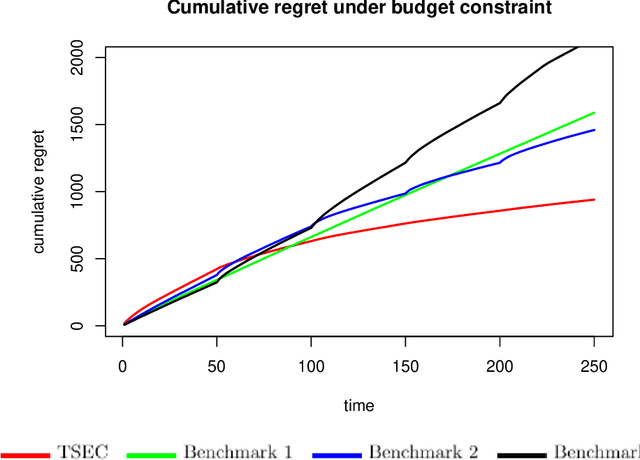

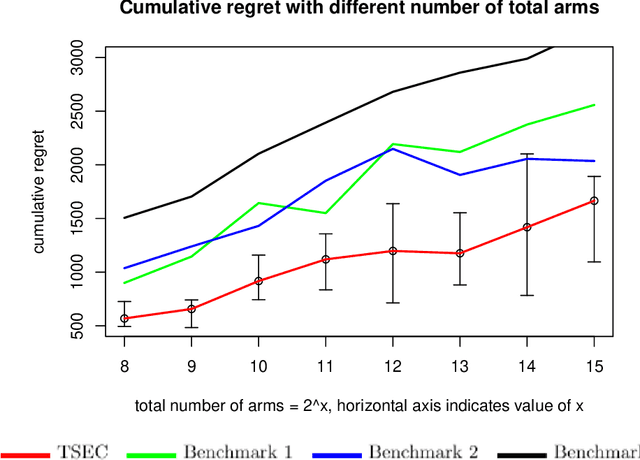

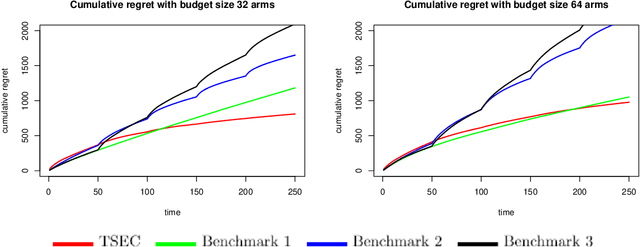

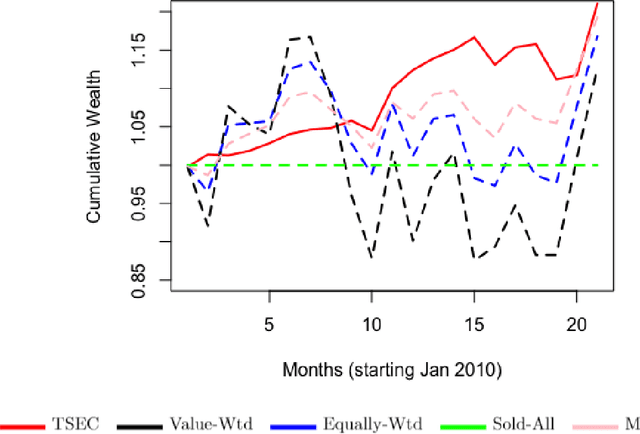

Thompson sampling is a popular algorithm for solving multi-armed bandit problems, and has been applied in a wide range of applications, from website design to portfolio optimization. In such applications, however, the number of choices (or arms) $N$ can be large, and the data needed to make adaptive decisions require expensive experimentation. One is then faced with the constraint of experimenting on only a small subset of $K \ll N$ arms within each time period, which poses a problem for traditional Thompson sampling. We propose a new Thompson Sampling under Experimental Constraints (TSEC) method, which addresses this so-called "arm budget constraint". TSEC makes use of a Bayesian interaction model with effect hierarchy priors, to model correlations between rewards on different arms. This fitted model is then integrated within Thompson sampling, to jointly identify a good subset of arms for experimentation and to allocate resources over these arms. We demonstrate the effectiveness of TSEC in two problems with arm budget constraints. The first is a simulated website optimization study, where TSEC shows noticeable improvements over industry benchmarks. The second is a portfolio optimization application on industry-based exchange-traded funds, where TSEC provides more consistent and greater wealth accumulation over standard investment strategies.