Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeUnpacking the Black Box: Regulating Algorithmic Decisions

Oct 05, 2021

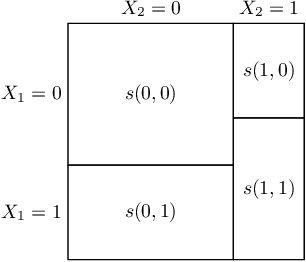

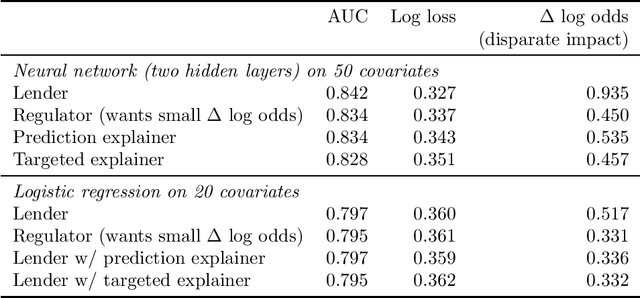

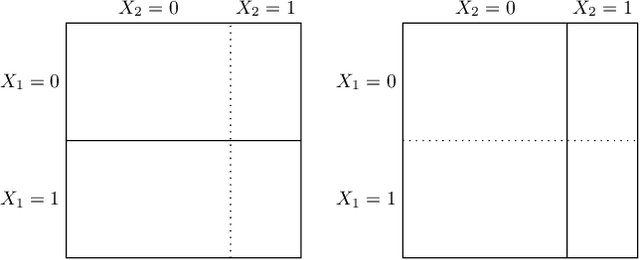

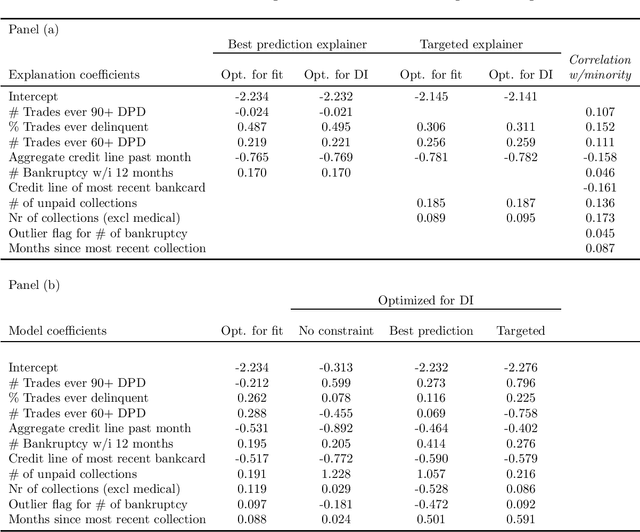

We characterize optimal oversight of algorithms in a world where an agent designs a complex prediction function but a principal is limited in the amount of information she can learn about the prediction function. We show that limiting agents to prediction functions that are simple enough to be fully transparent is inefficient as long as the bias induced by misalignment between principal's and agent's preferences is small relative to the uncertainty about the true state of the world. Algorithmic audits can improve welfare, but the gains depend on the design of the audit tools. Tools that focus on minimizing overall information loss, the focus of many post-hoc explainer tools, will generally be inefficient since they focus on explaining the average behavior of the prediction function rather than sources of mis-prediction, which matter for welfare-relevant outcomes. Targeted tools that focus on the source of incentive misalignment, e.g., excess false positives or racial disparities, can provide first-best solutions. We provide empirical support for our theoretical findings using an application in consumer lending.

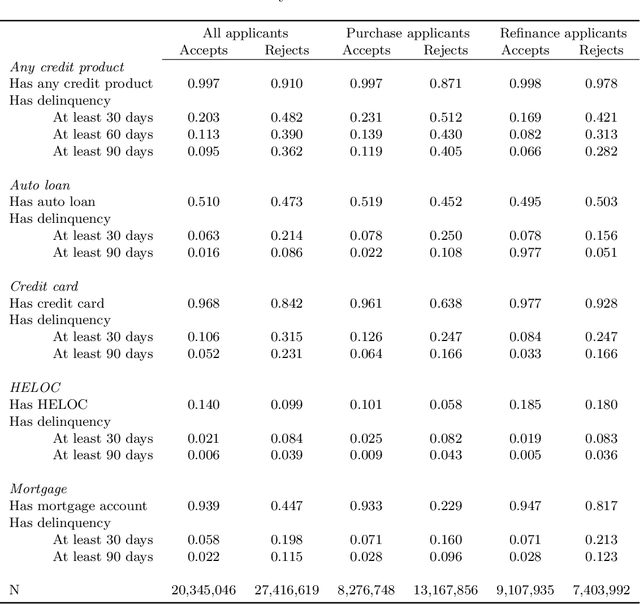

How Costly is Noise? Data and Disparities in Consumer Credit

May 17, 2021

We show that lenders face more uncertainty when assessing default risk of historically under-served groups in US credit markets and that this information disparity is a quantitatively important driver of inefficient and unequal credit market outcomes. We first document that widely used credit scores are statistically noisier indicators of default risk for historically under-served groups. This noise emerges primarily through the explanatory power of the underlying credit report data (e.g., thin credit files), not through issues with model fit (e.g., the inability to include protected class in the scoring model). Estimating a structural model of lending with heterogeneity in information, we quantify the gains from addressing these information disparities for the US mortgage market. We find that equalizing the precision of credit scores can reduce disparities in approval rates and in credit misallocation for disadvantaged groups by approximately half.