Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeDeep Learning Statistical Arbitrage

Jun 08, 2021

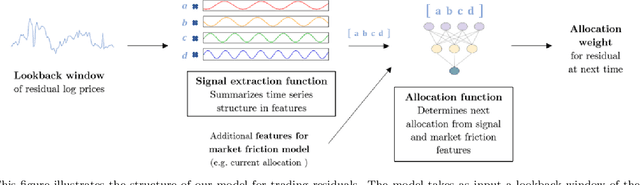

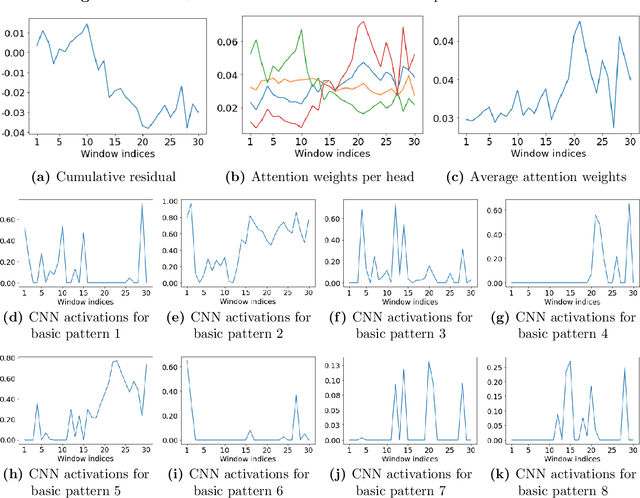

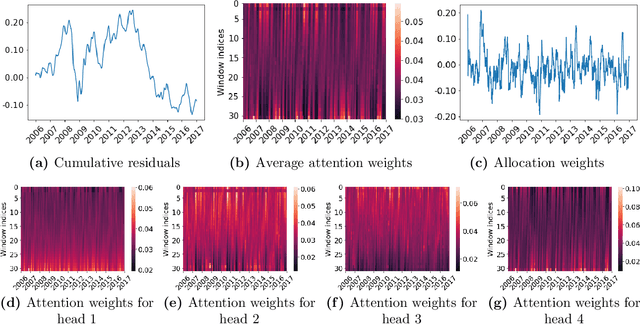

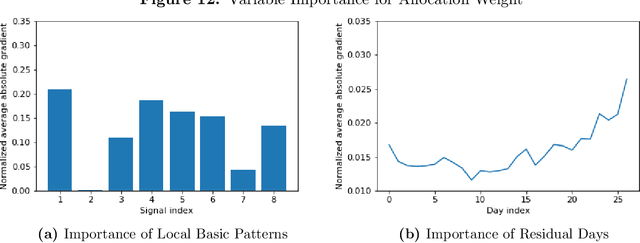

Statistical arbitrage identifies and exploits temporal price differences between similar assets. We propose a unifying conceptual framework for statistical arbitrage and develop a novel deep learning solution, which finds commonality and time-series patterns from large panels in a data-driven and flexible way. First, we construct arbitrage portfolios of similar assets as residual portfolios from conditional latent asset pricing factors. Second, we extract the time series signals of these residual portfolios with one of the most powerful machine learning time-series solutions, a convolutional transformer. Last, we use these signals to form an optimal trading policy, that maximizes risk-adjusted returns under constraints. We conduct a comprehensive empirical comparison study with daily large cap U.S. stocks. Our optimal trading strategy obtains a consistently high out-of-sample Sharpe ratio and substantially outperforms all benchmark approaches. It is orthogonal to common risk factors, and exploits asymmetric local trend and reversion patterns. Our strategies remain profitable after taking into account trading frictions and costs. Our findings suggest a high compensation for arbitrageurs to enforce the law of one price.