Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeExponentiated Subgradient Algorithm for Online Optimization under the Random Permutation Model

Feb 05, 2015

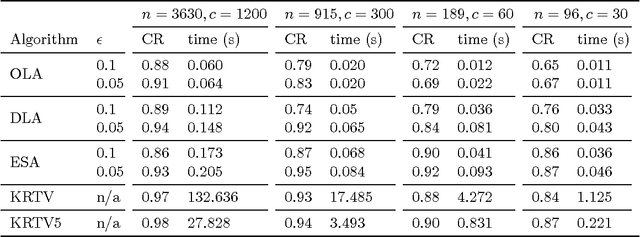

Online optimization problems arise in many resource allocation tasks, where the future demands for each resource and the associated utility functions change over time and are not known apriori, yet resources need to be allocated at every point in time despite the future uncertainty. In this paper, we consider online optimization problems with general concave utilities. We modify and extend an online optimization algorithm proposed by Devanur et al. for linear programming to this general setting. The model we use for the arrival of the utilities and demands is known as the random permutation model, where a fixed collection of utilities and demands are presented to the algorithm in random order. We prove that under this model the algorithm achieves a competitive ratio of $1-O(\epsilon)$ under a near-optimal assumption that the bid to budget ratio is $O (\frac{\epsilon^2}{\log({m}/{\epsilon})})$, where $m$ is the number of resources, while enjoying a significantly lower computational cost than the optimal algorithm proposed by Kesselheim et al. We draw a connection between the proposed algorithm and subgradient methods used in convex optimization. In addition, we present numerical experiments that demonstrate the performance and speed of this algorithm in comparison to existing algorithms.