Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeLogistic Ensemble Models

Jun 12, 2018

Predictive models that are developed in a regulated industry or a regulated application, like determination of credit worthiness, must be interpretable and rational (e.g., meaningful improvements in basic credit behavior must result in improved credit worthiness scores). Machine Learning technologies provide very good performance with minimal analyst intervention, making them well suited to a high volume analytic environment, but the majority are black box tools that provide very limited insight or interpretability into key drivers of model performance or predicted model output values. This paper presents a methodology that blends one of the most popular predictive statistical modeling methods for binary classification with a core model enhancement strategy found in machine learning. The resulting prediction methodology provides solid performance, from minimal analyst effort, while providing the interpretability and rationality required in regulated industries, as well as in other environments where interpretation of model parameters is required (e.g. businesses that require interpretation of models, to take action on them).

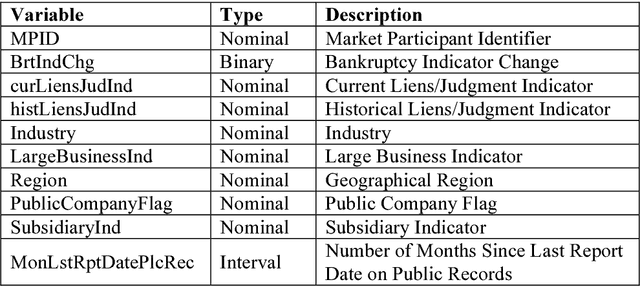

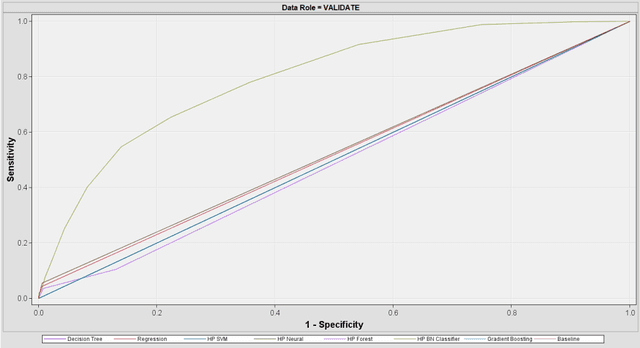

Influence of the Event Rate on Discrimination Abilities of Bankruptcy Prediction Models

Mar 10, 2018

In bankruptcy prediction, the proportion of events is very low, which is often oversampled to eliminate this bias. In this paper, we study the influence of the event rate on discrimination abilities of bankruptcy prediction models. First the statistical association and significance of public records and firmographics indicators with the bankruptcy were explored. Then the event rate was oversampled from 0.12% to 10%, 20%, 30%, 40%, and 50%, respectively. Seven models were developed, including Logistic Regression, Decision Tree, Random Forest, Gradient Boosting, Support Vector Machine, Bayesian Network, and Neural Network. Under different event rates, models were comprehensively evaluated and compared based on Kolmogorov-Smirnov Statistic, accuracy, F1 score, Type I error, Type II error, and ROC curve on the hold-out dataset with their best probability cut-offs. Results show that Bayesian Network is the most insensitive to the event rate, while Support Vector Machine is the most sensitive.