Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeInfluence of the Event Rate on Discrimination Abilities of Bankruptcy Prediction Models

Paper and Code

Mar 10, 2018

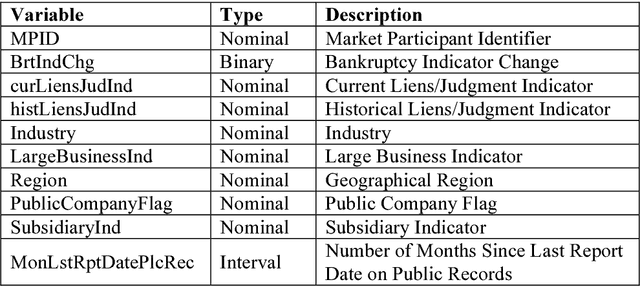

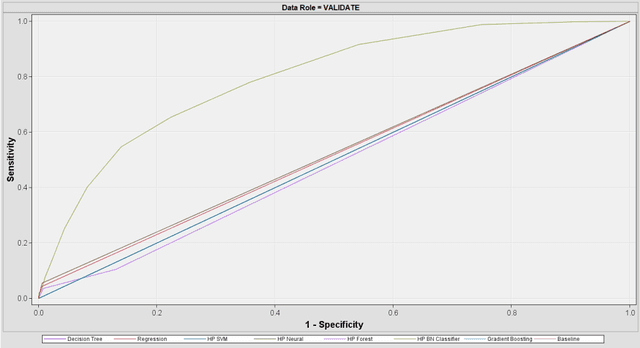

In bankruptcy prediction, the proportion of events is very low, which is often oversampled to eliminate this bias. In this paper, we study the influence of the event rate on discrimination abilities of bankruptcy prediction models. First the statistical association and significance of public records and firmographics indicators with the bankruptcy were explored. Then the event rate was oversampled from 0.12% to 10%, 20%, 30%, 40%, and 50%, respectively. Seven models were developed, including Logistic Regression, Decision Tree, Random Forest, Gradient Boosting, Support Vector Machine, Bayesian Network, and Neural Network. Under different event rates, models were comprehensively evaluated and compared based on Kolmogorov-Smirnov Statistic, accuracy, F1 score, Type I error, Type II error, and ROC curve on the hold-out dataset with their best probability cut-offs. Results show that Bayesian Network is the most insensitive to the event rate, while Support Vector Machine is the most sensitive.