Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeTime Series Anomaly Detection with label-free Model Selection

Jun 11, 2021

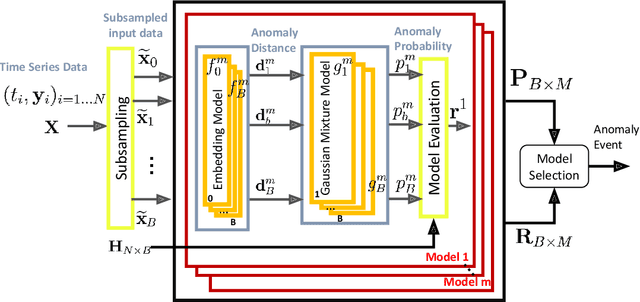

Anomaly detection for time-series data becomes an essential task for many data-driven applications fueled with an abundance of data and out-of-the-box machine-learning algorithms. In many real-world settings, developing a reliable anomaly model is highly challenging due to insufficient anomaly labels and the prohibitively expensive cost of obtaining anomaly examples. It imposes a significant bottleneck to evaluate model quality for model selection and parameter tuning reliably. As a result, many existing anomaly detection algorithms fail to show their promised performance after deployment. In this paper, we propose LaF-AD, a novel anomaly detection algorithm with label-free model selection for unlabeled times-series data. Our proposed algorithm performs a fully unsupervised ensemble learning across a large number of candidate parametric models. We develop a model variance metric that quantifies the sensitivity of anomaly probability with a bootstrapping method. Then it makes a collective decision for anomaly events by model learners using the model variance. Our algorithm is easily parallelizable, more robust for ill-conditioned and seasonal data, and highly scalable for a large number of anomaly models. We evaluate our algorithm against other state-of-the-art methods on a synthetic domain and a benchmark public data set.