Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeHigh-speed detection of emergent market clustering via an unsupervised parallel genetic algorithm

Aug 02, 2015

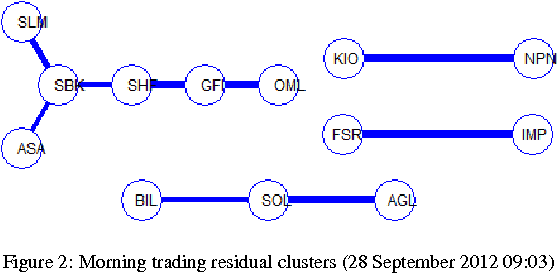

We implement a master-slave parallel genetic algorithm (PGA) with a bespoke log-likelihood fitness function to identify emergent clusters within price evolutions. We use graphics processing units (GPUs) to implement a PGA and visualise the results using disjoint minimal spanning trees (MSTs). We demonstrate that our GPU PGA, implemented on a commercially available general purpose GPU, is able to recover stock clusters in sub-second speed, based on a subset of stocks in the South African market. This represents a pragmatic choice for low-cost, scalable parallel computing and is significantly faster than a prototype serial implementation in an optimised C-based fourth-generation programming language, although the results are not directly comparable due to compiler differences. Combined with fast online intraday correlation matrix estimation from high frequency data for cluster identification, the proposed implementation offers cost-effective, near-real-time risk assessment for financial practitioners.

* 10 pages, 5 figures, 4 tables, More thorough discussion of implementation