Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeBayesian Inference on Matrix Manifolds for Linear Dimensionality Reduction

Jun 14, 2016

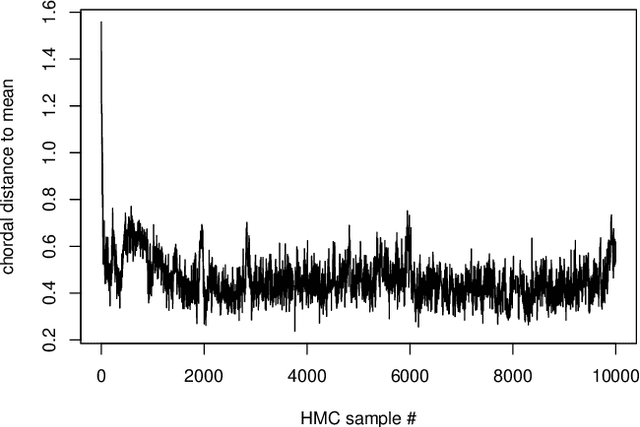

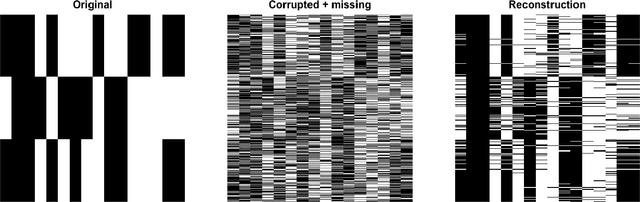

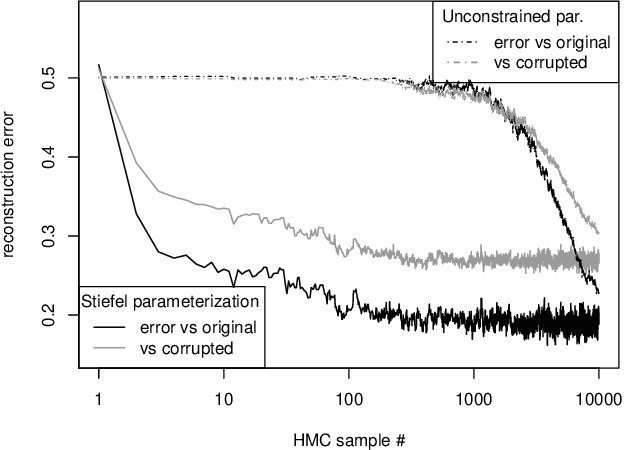

We reframe linear dimensionality reduction as a problem of Bayesian inference on matrix manifolds. This natural paradigm extends the Bayesian framework to dimensionality reduction tasks in higher dimensions with simpler models at greater speeds. Here an orthogonal basis is treated as a single point on a manifold and is associated with a linear subspace on which observations vary maximally. Throughout this paper, we employ the Grassmann and Stiefel manifolds for various dimensionality reduction problems, explore the connection between the two manifolds, and use Hybrid Monte Carlo for posterior sampling on the Grassmannian for the first time. We delineate in which situations either manifold should be considered. Further, matrix manifold models are used to yield scientific insight in the context of cognitive neuroscience, and we conclude that our methods are suitable for basic inference as well as accurate prediction.

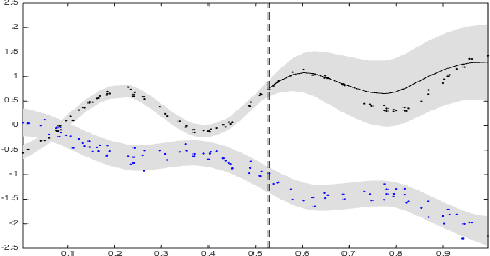

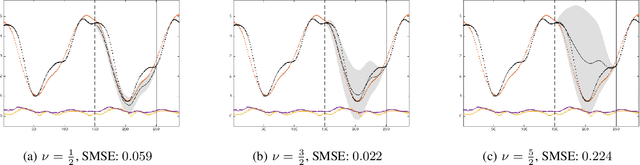

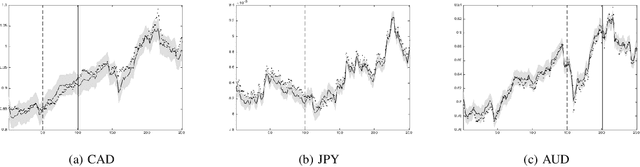

Dependent Matérn Processes for Multivariate Time Series

Feb 11, 2015

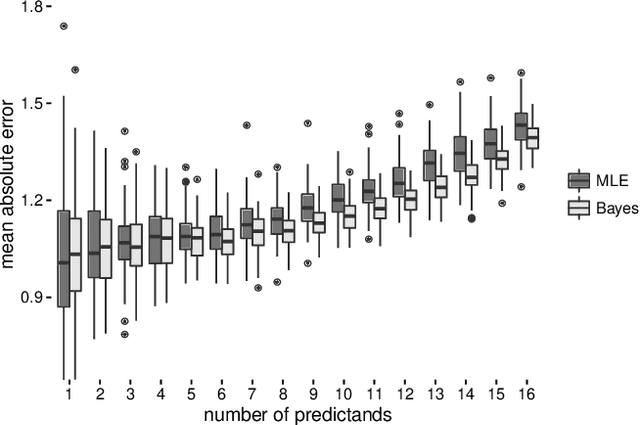

For the challenging task of modeling multivariate time series, we propose a new class of models that use dependent Mat\'ern processes to capture the underlying structure of data, explain their interdependencies, and predict their unknown values. Although similar models have been proposed in the econometric, statistics, and machine learning literature, our approach has several advantages that distinguish it from existing methods: 1) it is flexible to provide high prediction accuracy, yet its complexity is controlled to avoid overfitting; 2) its interpretability separates it from black-box methods; 3) finally, its computational efficiency makes it scalable for high-dimensional time series. In this paper, we use several simulated and real data sets to illustrate these advantages. We will also briefly discuss some extensions of our model.