Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeDependent Matérn Processes for Multivariate Time Series

Paper and Code

Feb 11, 2015

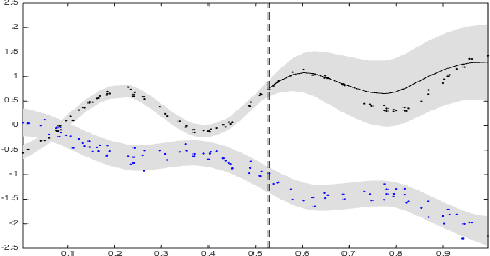

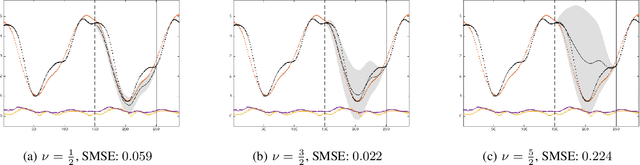

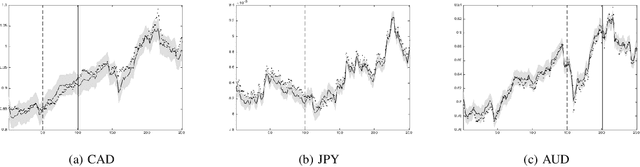

For the challenging task of modeling multivariate time series, we propose a new class of models that use dependent Mat\'ern processes to capture the underlying structure of data, explain their interdependencies, and predict their unknown values. Although similar models have been proposed in the econometric, statistics, and machine learning literature, our approach has several advantages that distinguish it from existing methods: 1) it is flexible to provide high prediction accuracy, yet its complexity is controlled to avoid overfitting; 2) its interpretability separates it from black-box methods; 3) finally, its computational efficiency makes it scalable for high-dimensional time series. In this paper, we use several simulated and real data sets to illustrate these advantages. We will also briefly discuss some extensions of our model.