Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeThe value of text for small business default prediction: A deep learning approach

Paper and Code

Mar 19, 2020

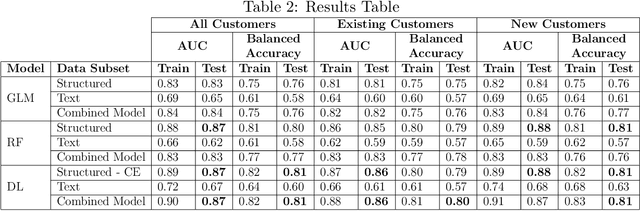

Compared to consumer lending, Micro, Small and Medium Enterprise (mSME) credit risk modelling is particularly challenging, as, often, the same sources of information are not available. To mitigate limited data availability, it is standard policy for a loan officer to provide a textual loan assessment. In turn, this statement is analysed by a credit expert alongside any available standard credit data. In our paper, we exploit recent advances from the field of Deep Learning and Natural Language Processing (NLP), including the BERT (Bidirectional Encoder Representations from Transformers) model, to extract information from 60000+ textual assessments. We consider the performance in terms of AUC (Area Under the Curve) and Balanced Accuracy and find that the text alone is surprisingly effective for predicting default. Yet, when combined with traditional data, it yields no additional predictive capability. We do find, however, that deep learning with categorical embeddings is capable of producing a modest performance improvement when compared to alternative machine learning models. We explore how the loan assessments influence predictions, explaining why despite the text being predictive, no additional performance is gained. This exploration leads us to a series of recommendations on a new strategy for the collection of future mSME loan assessments.