Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeThe Parametric Cost Function Approximation: A new approach for multistage stochastic programming

Paper and Code

Jan 01, 2022

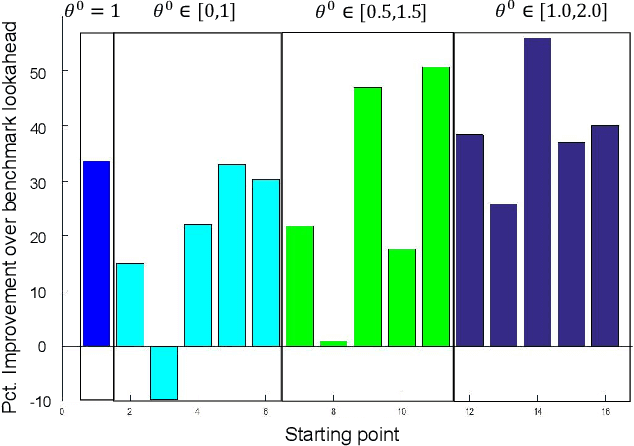

The most common approaches for solving multistage stochastic programming problems in the research literature have been to either use value functions ("dynamic programming") or scenario trees ("stochastic programming") to approximate the impact of a decision now on the future. By contrast, common industry practice is to use a deterministic approximation of the future which is easier to understand and solve, but which is criticized for ignoring uncertainty. We show that a parameterized version of a deterministic optimization model can be an effective way of handling uncertainty without the complexity of either stochastic programming or dynamic programming. We present the idea of a parameterized deterministic optimization model, and in particular a deterministic lookahead model, as a powerful strategy for many complex stochastic decision problems. This approach can handle complex, high-dimensional state variables, and avoids the usual approximations associated with scenario trees or value function approximations. Instead, it introduces the offline challenge of designing and tuning the parameterization. We illustrate the idea by using a series of application settings, and demonstrate its use in a nonstationary energy storage problem with rolling forecasts.