Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

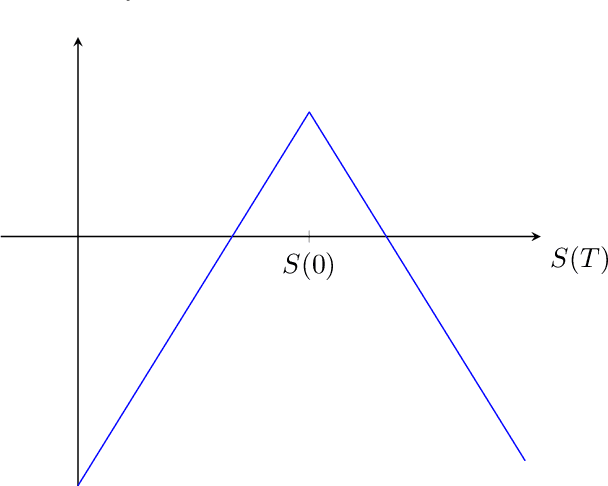

Add to EdgeSupervised machine learning classification for short straddles on the S&P500

Paper and Code

Apr 26, 2022

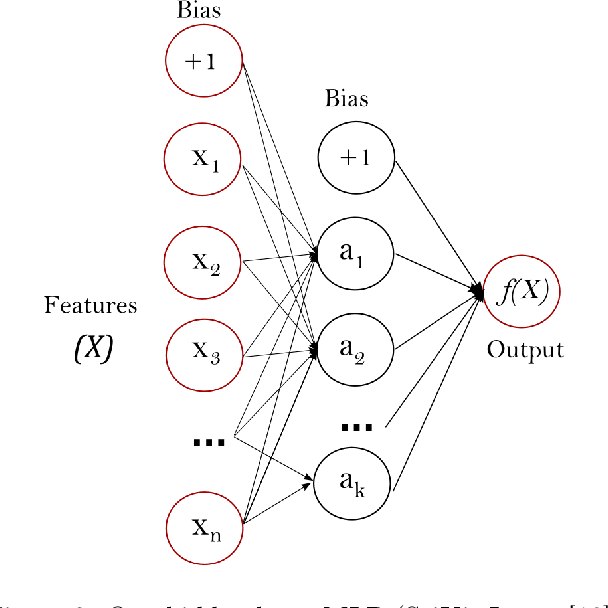

In this working paper we present our current progress in the training of machine learning models to execute short option strategies on the S&P500. As a first step, this paper is breaking this problem down to a supervised classification task to decide if a short straddle on the S&P500 should be executed or not on a daily basis. We describe our used framework and present an overview over our evaluation metrics on different classification models. In this preliminary work, using standard machine learning techniques and without hyperparameter search, we find no statistically significant outperformance to a simple "trade always" strategy, but gain additional insights on how we could proceed in further experiments.

* 25 pages

View paper on