Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeStock Trading Optimization through Model-based Reinforcement Learning with Resistance Support Relative Strength

Paper and Code

May 30, 2022

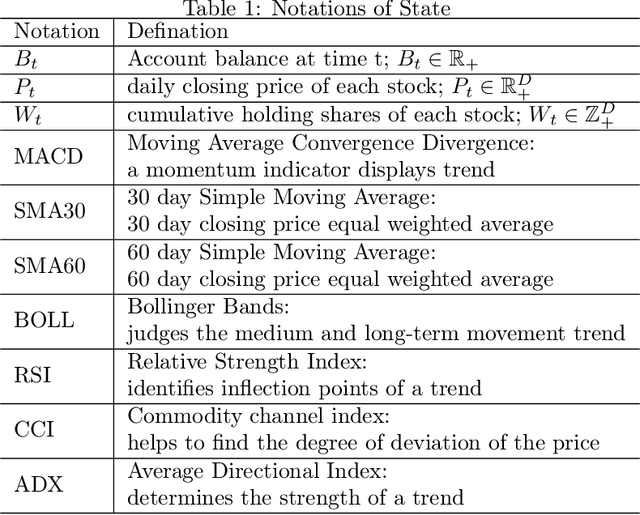

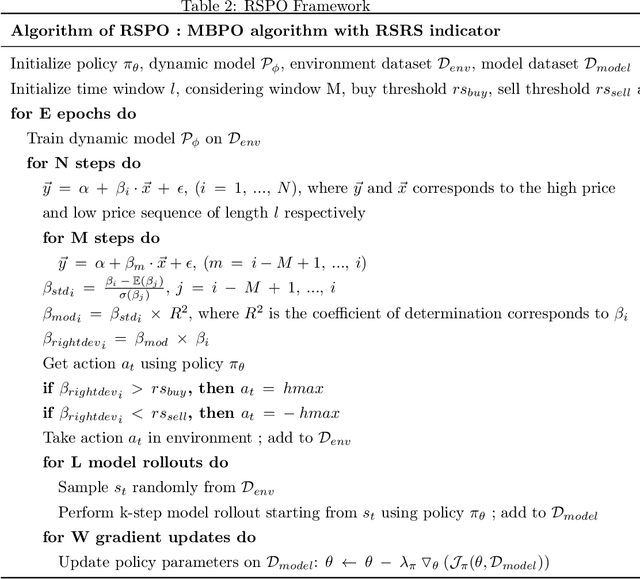

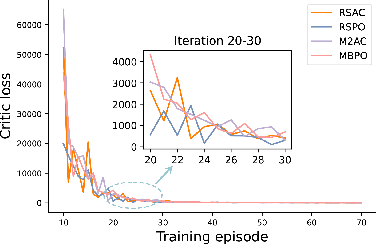

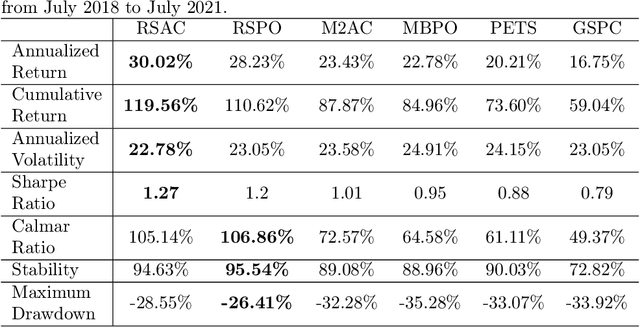

Reinforcement learning (RL) is gaining attention by more and more researchers in quantitative finance as the agent-environment interaction framework is aligned with decision making process in many business problems. Most of the current financial applications using RL algorithms are based on model-free method, which still faces stability and adaptivity challenges. As lots of cutting-edge model-based reinforcement learning (MBRL) algorithms mature in applications such as video games or robotics, we design a new approach that leverages resistance and support (RS) level as regularization terms for action in MBRL, to improve the algorithm's efficiency and stability. From the experiment results, we can see RS level, as a market timing technique, enhances the performance of pure MBRL models in terms of various measurements and obtains better profit gain with less riskiness. Besides, our proposed method even resists big drop (less maximum drawdown) during COVID-19 pandemic period when the financial market got unpredictable crisis. Explanations on why control of resistance and support level can boost MBRL is also investigated through numerical experiments, such as loss of actor-critic network and prediction error of the transition dynamical model. It shows that RS indicators indeed help the MBRL algorithms to converge faster at early stage and obtain smaller critic loss as training episodes increase.