Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeStage-wise Conservative Linear Bandits

Paper and Code

Sep 30, 2020

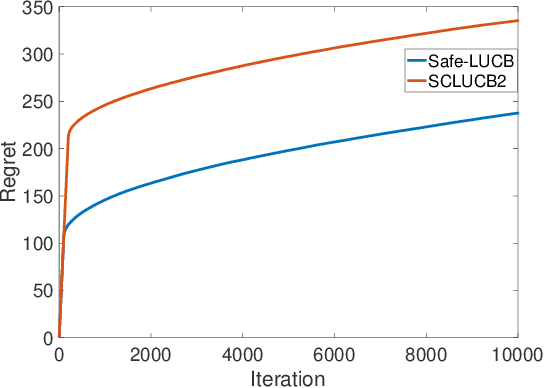

We study stage-wise conservative linear stochastic bandits: an instance of bandit optimization, which accounts for (unknown) safety constraints that appear in applications such as online advertising and medical trials. At each stage, the learner must choose actions that not only maximize cumulative reward across the entire time horizon but further satisfy a linear baseline constraint that takes the form of a lower bound on the instantaneous reward. For this problem, we present two novel algorithms, stage-wise conservative linear Thompson Sampling (SCLTS) and stage-wise conservative linear UCB (SCLUCB), that respect the baseline constraints and enjoy probabilistic regret bounds of order O(\sqrt{T} \log^{3/2}T) and O(\sqrt{T} \log T), respectively. Notably, the proposed algorithms can be adjusted with only minor modifications to tackle different problem variations, such as constraints with bandit-feedback, or an unknown sequence of baseline actions. We discuss these and other improvements over the state-of-the-art. For instance, compared to existing solutions, we show that SCLTS plays the (non-optimal) baseline action at most O(\log{T}) times (compared to O(\sqrt{T})). Finally, we make connections to another studied form of safety constraints that takes the form of an upper bound on the instantaneous reward. While this incurs additional complexity to the learning process as the optimal action is not guaranteed to belong to the safe set at each round, we show that SCLUCB can properly adjust in this setting via a simple modification.