Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeSimultaneously Solving FBSDEs with Neural Operators of Logarithmic Depth, Constant Width, and Sub-Linear Rank

Paper and Code

Oct 18, 2024

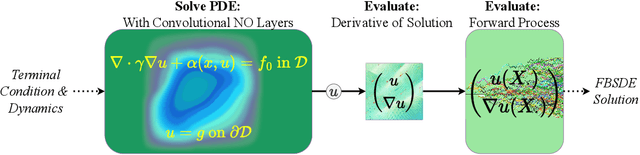

Forward-backwards stochastic differential equations (FBSDEs) are central in optimal control, game theory, economics, and mathematical finance. Unfortunately, the available FBSDE solvers operate on \textit{individual} FBSDEs, meaning that they cannot provide a computationally feasible strategy for solving large families of FBSDEs as these solvers must be re-run several times. \textit{Neural operators} (NOs) offer an alternative approach for \textit{simultaneously solving} large families of FBSDEs by directly approximating the solution operator mapping \textit{inputs:} terminal conditions and dynamics of the backwards process to \textit{outputs:} solutions to the associated FBSDE. Though universal approximation theorems (UATs) guarantee the existence of such NOs, these NOs are unrealistically large. We confirm that ``small'' NOs can uniformly approximate the solution operator to structured families of FBSDEs with random terminal time, uniformly on suitable compact sets determined by Sobolev norms, to any prescribed error $\varepsilon>0$ using a depth of $\mathcal{O}(\log(1/\varepsilon))$, a width of $\mathcal{O}(1)$, and a sub-linear rank; i.e. $\mathcal{O}(1/\varepsilon^r)$ for some $r<1$. This result is rooted in our second main contribution, which shows that convolutional NOs of similar depth, width, and rank can approximate the solution operator to a broad class of Elliptic PDEs. A key insight here is that the convolutional layers of our NO can efficiently encode the Green's function associated to the Elliptic PDEs linked to our FBSDEs. A byproduct of our analysis is the first theoretical justification for the benefit of lifting channels in NOs: they exponentially decelerate the growth rate of the NO's rank.