Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeSimulation-Informed Revenue Extrapolation with Confidence Estimate for Scaleup Companies Using Scarce Time-Series Data

Paper and Code

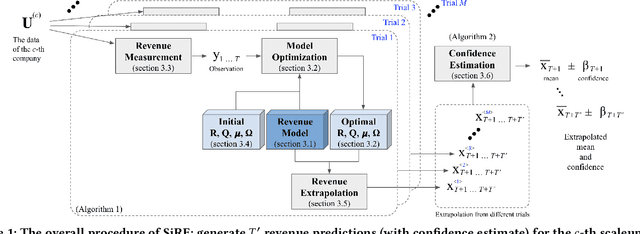

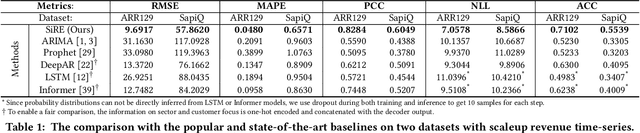

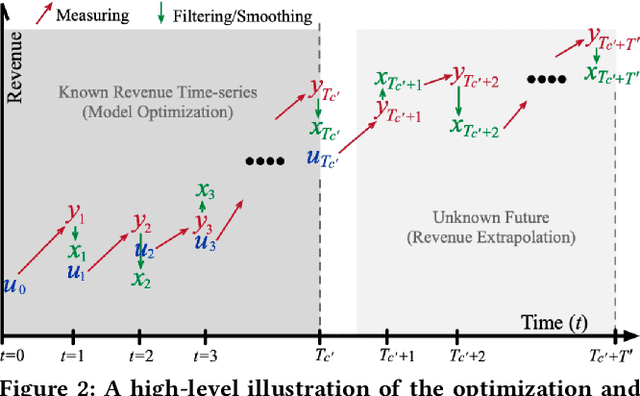

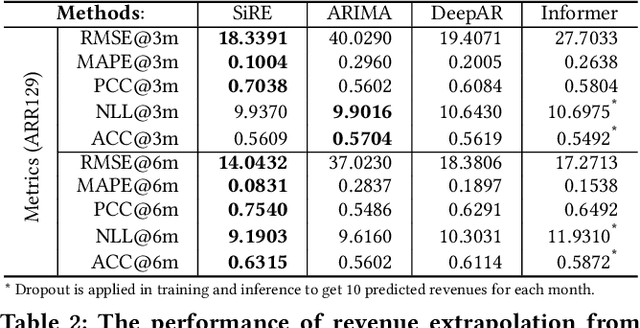

Investment professionals rely on extrapolating company revenue into the future (i.e. revenue forecast) to approximate the valuation of scaleups (private companies in a high-growth stage) and inform their investment decision. This task is manual and empirical, leaving the forecast quality heavily dependent on the investment professionals' experiences and insights. Furthermore, financial data on scaleups is typically proprietary, costly and scarce, ruling out the wide adoption of data-driven approaches. To this end, we propose a simulation-informed revenue extrapolation (SiRE) algorithm that generates fine-grained long-term revenue predictions on small datasets and short time-series. SiRE models the revenue dynamics as a linear dynamical system (LDS), which is solved using the EM algorithm. The main innovation lies in how the noisy revenue measurements are obtained during training and inferencing. SiRE works for scaleups that operate in various sectors and provides confidence estimates. The quantitative experiments on two practical tasks show that SiRE significantly surpasses the baseline methods by a large margin. We also observe high performance when SiRE extrapolates long-term predictions from short time-series. The performance-efficiency balance and result explainability of SiRE are also validated empirically. Evaluated from the perspective of investment professionals, SiRE can precisely locate the scaleups that have a great potential return in 2 to 5 years. Furthermore, our qualitative inspection illustrates some advantageous attributes of the SiRE revenue forecasts.