Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeSequential hypothesis testing in machine learning driven crude oil jump detection

Paper and Code

Apr 19, 2020

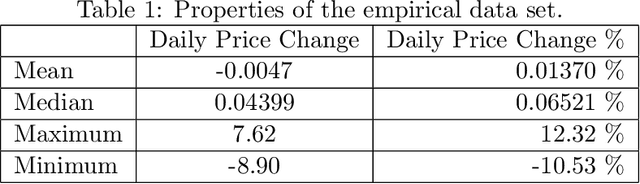

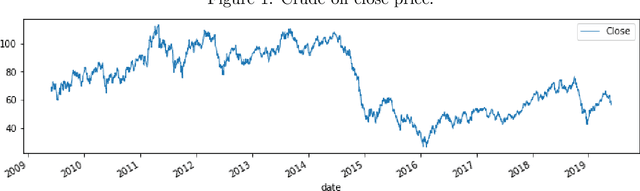

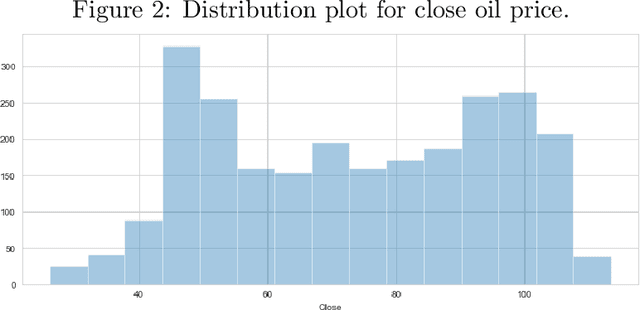

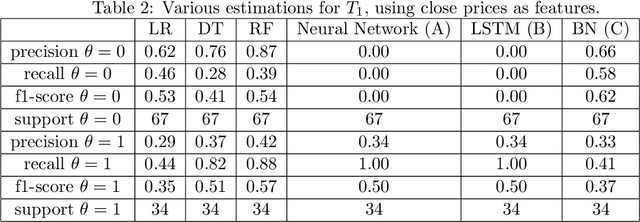

In this paper we present a sequential hypothesis test for the detection of general jump size distrubution. Infinitesimal generators for the corresponding log-likelihood ratios are presented and analyzed. Bounds for infinitesimal generators in terms of super-solutions and sub-solutions are computed. This is shown to be implementable in relation to various classification problems for a crude oil price data set. Machine and deep learning algorithms are implemented to extract a specific deterministic component from the crude oil data set, and the deterministic component is implemented to improve the Barndorff-Nielsen and Shephard model, a commonly used stochastic model for derivative and commodity market analysis.

* 23 pages, 5 figures

View paper on