Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeRobust $Q$-learning Algorithm for Markov Decision Processes under Wasserstein Uncertainty

Paper and Code

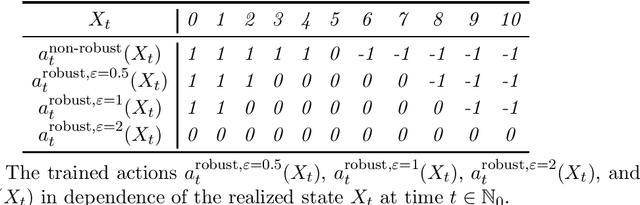

We present a novel $Q$-learning algorithm to solve distributionally robust Markov decision problems, where the corresponding ambiguity set of transition probabilities for the underlying Markov decision process is a Wasserstein ball around a (possibly estimated) reference measure. We prove convergence of the presented algorithm and provide several examples also using real data to illustrate both the tractability of our algorithm as well as the benefits of considering distributional robustness when solving stochastic optimal control problems, in particular when the estimated distributions turn out to be misspecified in practice.

View paper on