Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeRobust Multi-agent Counterfactual Prediction

Paper and Code

Apr 03, 2019

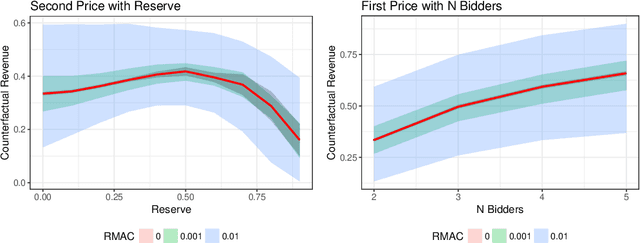

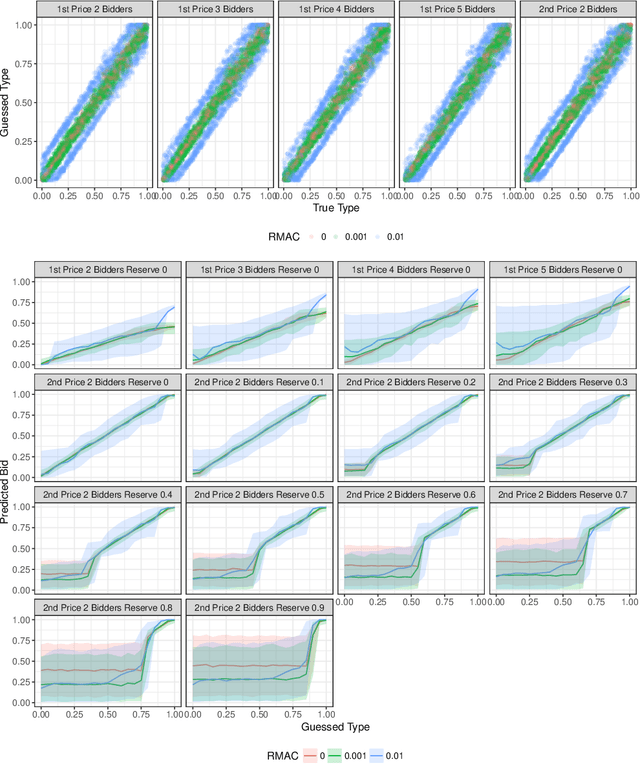

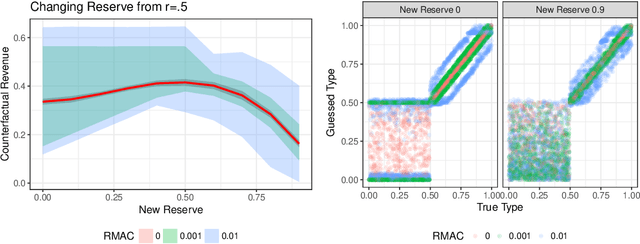

We consider the problem of using logged data to make predictions about what would happen if we changed the `rules of the game' in a multi-agent system. This task is difficult because in many cases we observe actions individuals take but not their private information or their full reward functions. In addition, agents are strategic, so when the rules change, they will also change their actions. Existing methods (e.g. structural estimation, inverse reinforcement learning) make counterfactual predictions by constructing a model of the game, adding the assumption that agents' behavior comes from optimizing given some goals, and then inverting observed actions to learn agent's underlying utility function (a.k.a. type). Once the agent types are known, making counterfactual predictions amounts to solving for the equilibrium of the counterfactual environment. This approach imposes heavy assumptions such as rationality of the agents being observed, correctness of the analyst's model of the environment/parametric form of the agents' utility functions, and various other conditions to make point identification possible. We propose a method for analyzing the sensitivity of counterfactual conclusions to violations of these assumptions. We refer to this method as robust multi-agent counterfactual prediction (RMAC). We apply our technique to investigating the robustness of counterfactual claims for classic environments in market design: auctions, school choice, and social choice. Importantly, we show RMAC can be used in regimes where point identification is impossible (e.g. those which have multiple equilibria or non-injective maps from type distributions to outcomes).