Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeRisk-Sensitive Markov Decision Processes with Long-Run CVaR Criterion

Paper and Code

Oct 17, 2022

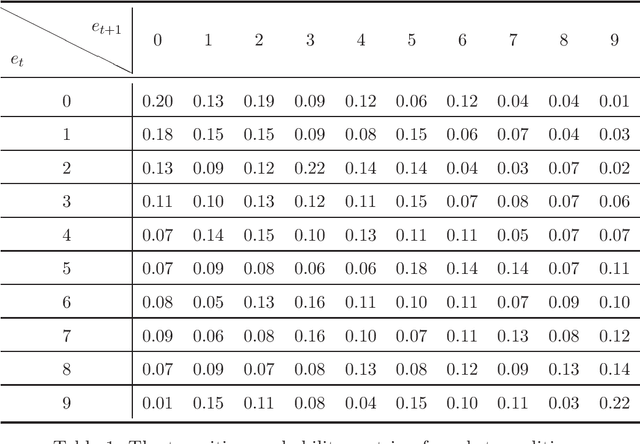

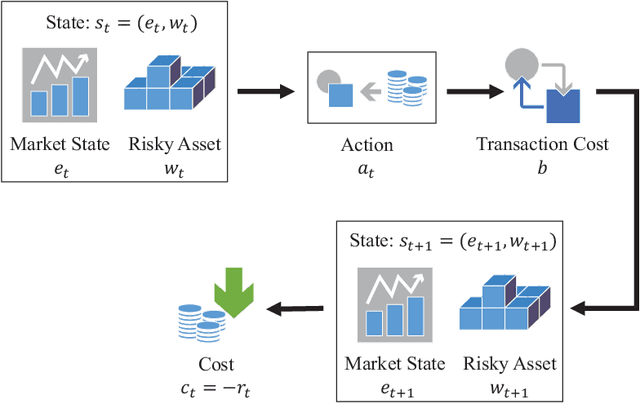

CVaR (Conditional Value at Risk) is a risk metric widely used in finance. However, dynamically optimizing CVaR is difficult since it is not a standard Markov decision process (MDP) and the principle of dynamic programming fails. In this paper, we study the infinite-horizon discrete-time MDP with a long-run CVaR criterion, from the view of sensitivity-based optimization. By introducing a pseudo CVaR metric, we derive a CVaR difference formula which quantifies the difference of long-run CVaR under any two policies. The optimality of deterministic policies is derived. We obtain a so-called Bellman local optimality equation for CVaR, which is a necessary and sufficient condition for local optimal policies and only necessary for global optimal policies. A CVaR derivative formula is also derived for providing more sensitivity information. Then we develop a policy iteration type algorithm to efficiently optimize CVaR, which is shown to converge to local optima in the mixed policy space. We further discuss some extensions including the mean-CVaR optimization and the maximization of CVaR. Finally, we conduct numerical experiments relating to portfolio management to demonstrate the main results. Our work may shed light on dynamically optimizing CVaR from a sensitivity viewpoint.