Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeRisk-Sensitive Compact Decision Trees for Autonomous Execution in Presence of Simulated Market Response

Paper and Code

Jun 05, 2019

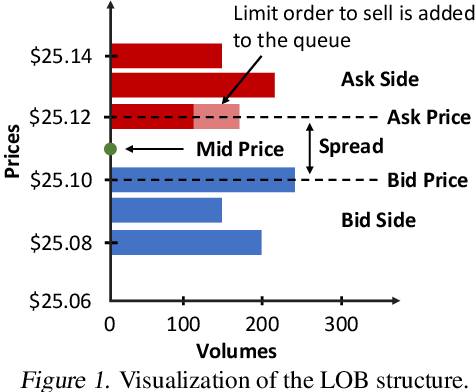

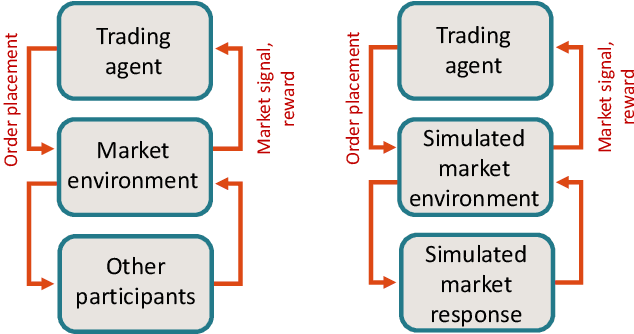

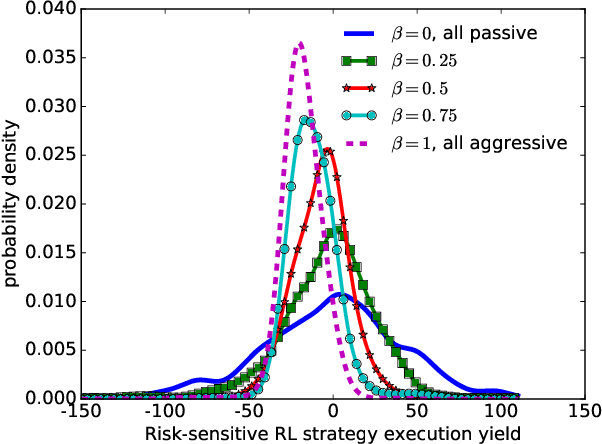

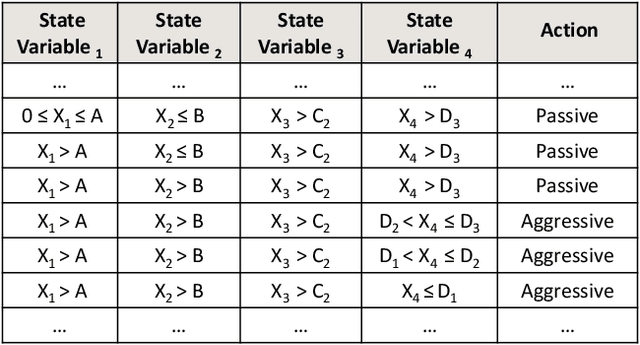

We demonstrate an application of risk-sensitive reinforcement learning to optimizing execution in limit order book markets. We represent taking order execution decisions based on limit order book knowledge by a Markov Decision Process; and train a trading agent in a market simulator, which emulates multi-agent interaction by synthesizing market response to our agent's execution decisions from historical data. Due to market impact, executing high volume orders can incur significant cost. We learn trading signals from market microstructure in presence of simulated market response and derive explainable decision-tree-based execution policies using risk-sensitive Q-learning to minimize execution cost subject to constraints on cost variance.

* Proceedings of the 36th International Conference on Machine

Learning,Long Beach, California, 2019

View paper on