Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeRevenue Optimization in Posted-Price Auctions with Strategic Buyers

Paper and Code

Nov 23, 2014

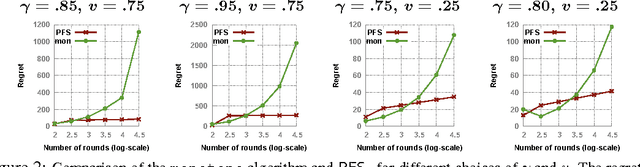

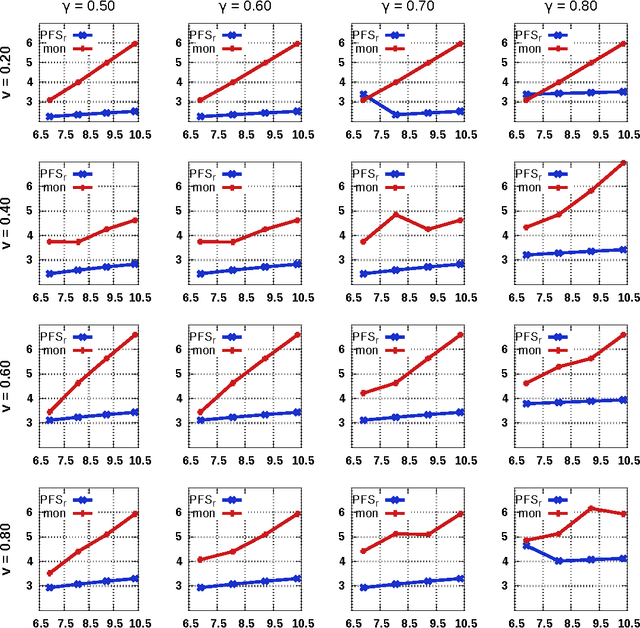

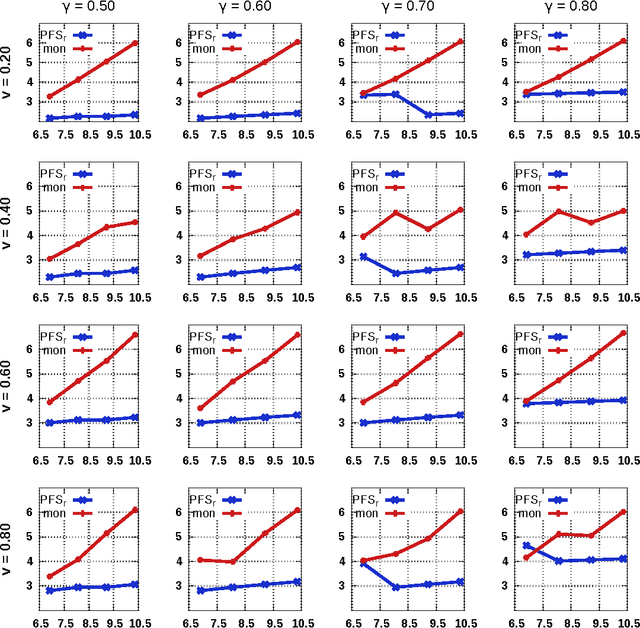

We study revenue optimization learning algorithms for posted-price auctions with strategic buyers. We analyze a very broad family of monotone regret minimization algorithms for this problem, which includes the previously best known algorithm, and show that no algorithm in that family admits a strategic regret more favorable than $\Omega(\sqrt{T})$. We then introduce a new algorithm that achieves a strategic regret differing from the lower bound only by a factor in $O(\log T)$, an exponential improvement upon the previous best algorithm. Our new algorithm admits a natural analysis and simpler proofs, and the ideas behind its design are general. We also report the results of empirical evaluations comparing our algorithm with the previous state of the art and show a consistent exponential improvement in several different scenarios.