Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeRank-one Convexification for Sparse Regression

Paper and Code

Jan 29, 2019

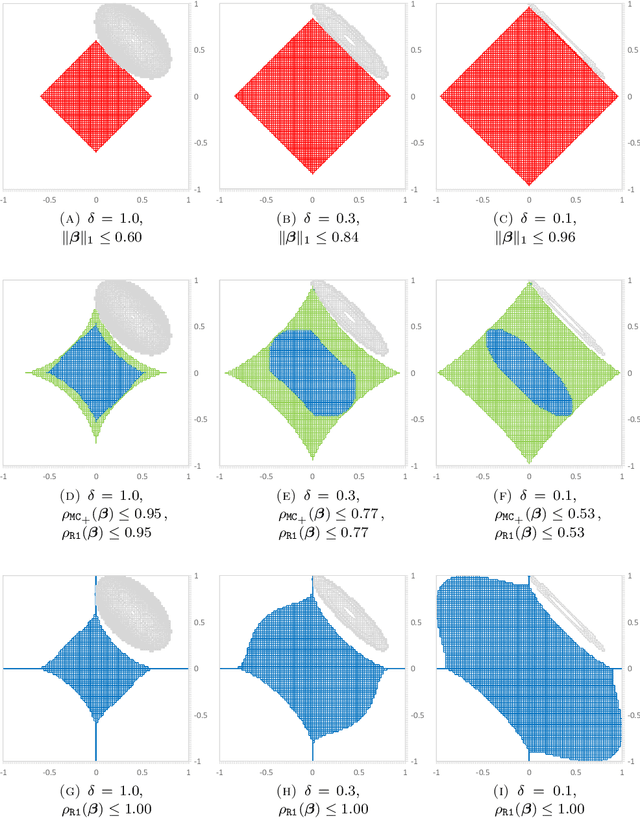

Sparse regression models are increasingly prevalent due to their ease of interpretability and superior out-of-sample performance. However, the exact model of sparse regression with an $\ell_0$ constraint restricting the support of the estimators is a challenging non-convex optimization problem. In this paper, we derive new strong convex relaxations for sparse regression. These relaxations are based on the ideal (convex-hull) formulations for rank-one quadratic terms with indicator variables. The new relaxations can be formulated as semidefinite optimization problems in an extended space and are stronger and more general than the state-of-the-art formulations, including the perspective reformulation and formulations with the reverse Huber penalty and the minimax concave penalty functions. Furthermore, the proposed rank-one strengthening can be interpreted as a non-separable, non-convex sparsity-inducing regularizer, which dynamically adjusts its penalty according to the shape of the error function. In our computational experiments with benchmark datasets, the proposed conic formulations are solved within seconds and result in near-optimal solutions (with 0.4\% optimality gap) for non-convex $\ell_0$-problems. Moreover, the resulting estimators also outperform alternative convex approaches from a statistical viewpoint, achieving high prediction accuracy and good interpretability.