Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeQuasi-Newton particle Metropolis-Hastings

Paper and Code

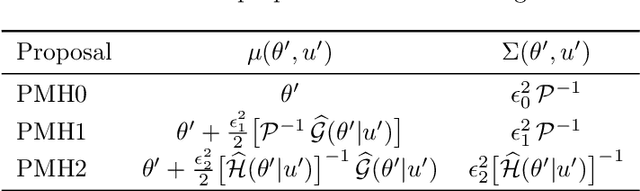

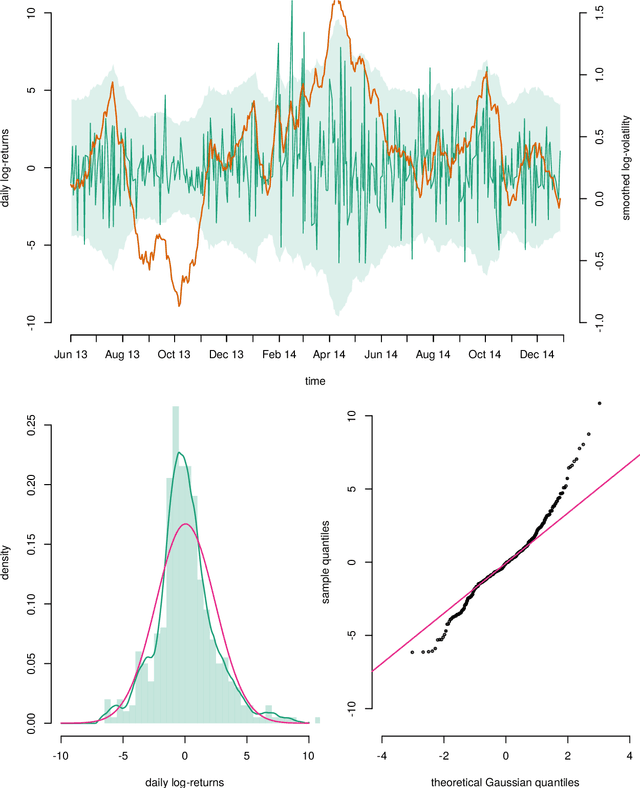

Particle Metropolis-Hastings enables Bayesian parameter inference in general nonlinear state space models (SSMs). However, in many implementations a random walk proposal is used and this can result in poor mixing if not tuned correctly using tedious pilot runs. Therefore, we consider a new proposal inspired by quasi-Newton algorithms that may achieve similar (or better) mixing with less tuning. An advantage compared to other Hessian based proposals, is that it only requires estimates of the gradient of the log-posterior. A possible application is parameter inference in the challenging class of SSMs with intractable likelihoods. We exemplify this application and the benefits of the new proposal by modelling log-returns of future contracts on coffee by a stochastic volatility model with $\alpha$-stable observations.