Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeOn LASSO for High Dimensional Predictive Regression

Paper and Code

Dec 14, 2022

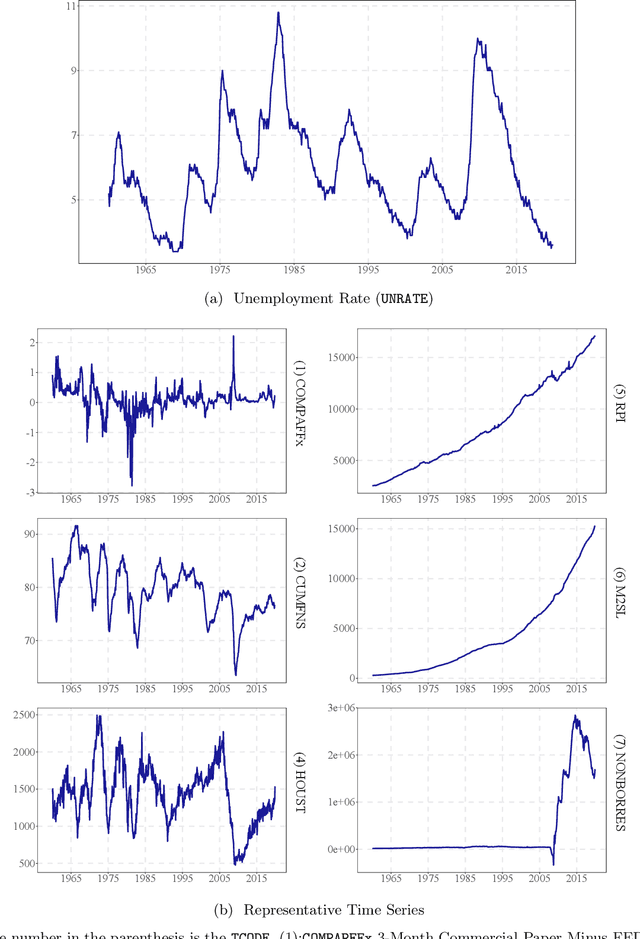

In a high dimensional linear predictive regression where the number of potential predictors can be larger than the sample size, we consider using LASSO, a popular L1-penalized regression method, to estimate the sparse coefficients when many unit root regressors are present. Consistency of LASSO relies on two building blocks: the deviation bound of the cross product of the regressors and the error term, and the restricted eigenvalue of the Gram matrix of the regressors. In our setting where unit root regressors are driven by temporal dependent non-Gaussian innovations, we establish original probabilistic bounds for these two building blocks. The bounds imply that the rates of convergence of LASSO are different from those in the familiar cross sectional case. In practical applications given a mixture of stationary and nonstationary predictors, asymptotic guarantee of LASSO is preserved if all predictors are scale-standardized. In an empirical example of forecasting the unemployment rate with many macroeconomic time series, strong performance is delivered by LASSO when the initial specification is guided by macroeconomic domain expertise.