Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeMining the Web for the Voice of the Herd to Track Stock Market Bubbles

Paper and Code

Dec 11, 2012

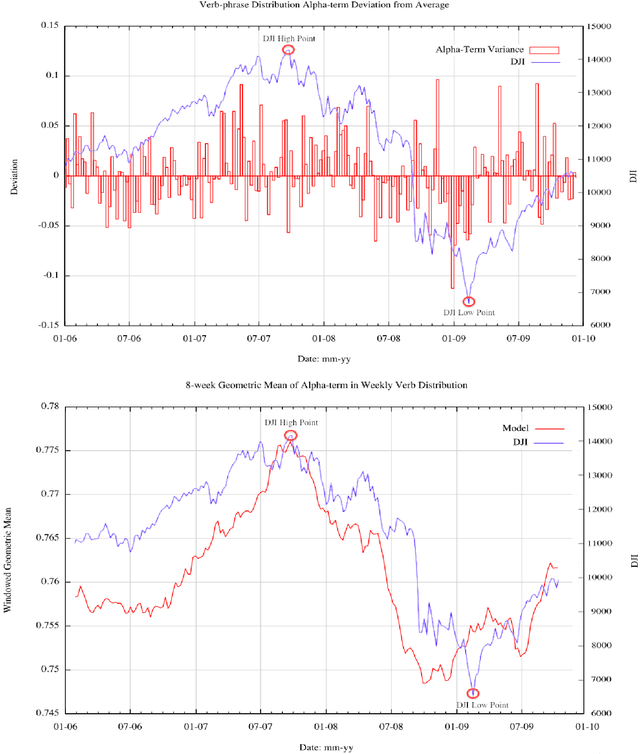

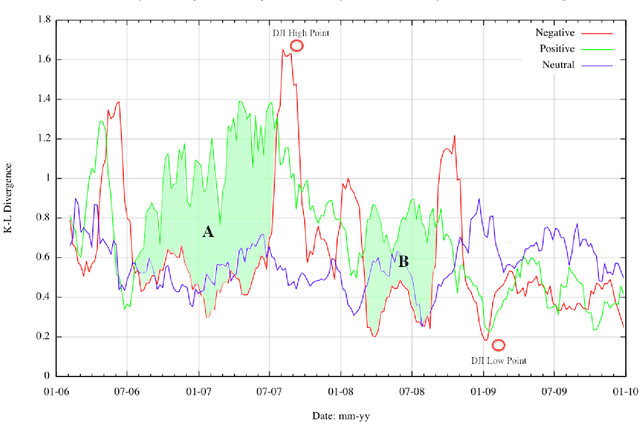

We show that power-law analyses of financial commentaries from newspaper web-sites can be used to identify stock market bubbles, supplementing traditional volatility analyses. Using a four-year corpus of 17,713 online, finance-related articles (10M+ words) from the Financial Times, the New York Times, and the BBC, we show that week-to-week changes in power-law distributions reflect market movements of the Dow Jones Industrial Average (DJI), the FTSE-100, and the NIKKEI-225. Notably, the statistical regularities in language track the 2007 stock market bubble, showing emerging structure in the language of commentators, as progressively greater agreement arose in their positive perceptions of the market. Furthermore, during the bubble period, a marked divergence in positive language occurs as revealed by a Kullback-Leibler analysis.