Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeMarkovian RNN: An Adaptive Time Series Prediction Network with HMM-based Switching for Nonstationary Environments

Paper and Code

Jun 17, 2020

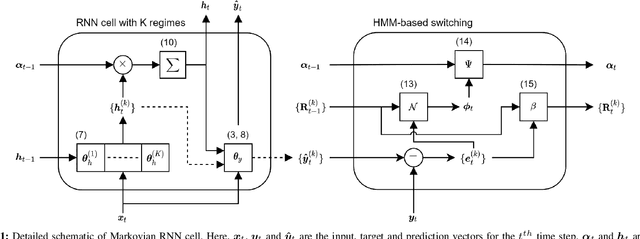

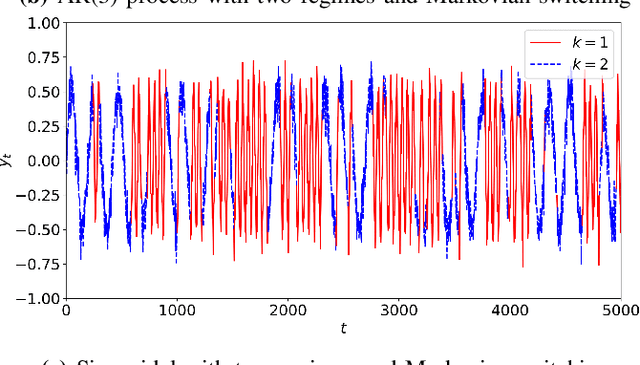

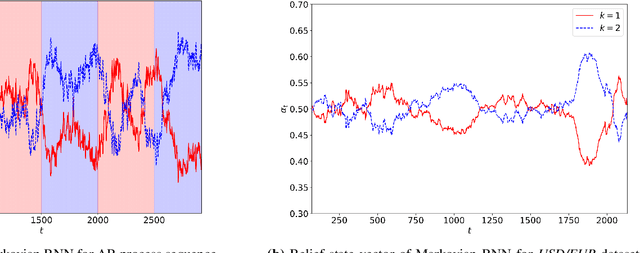

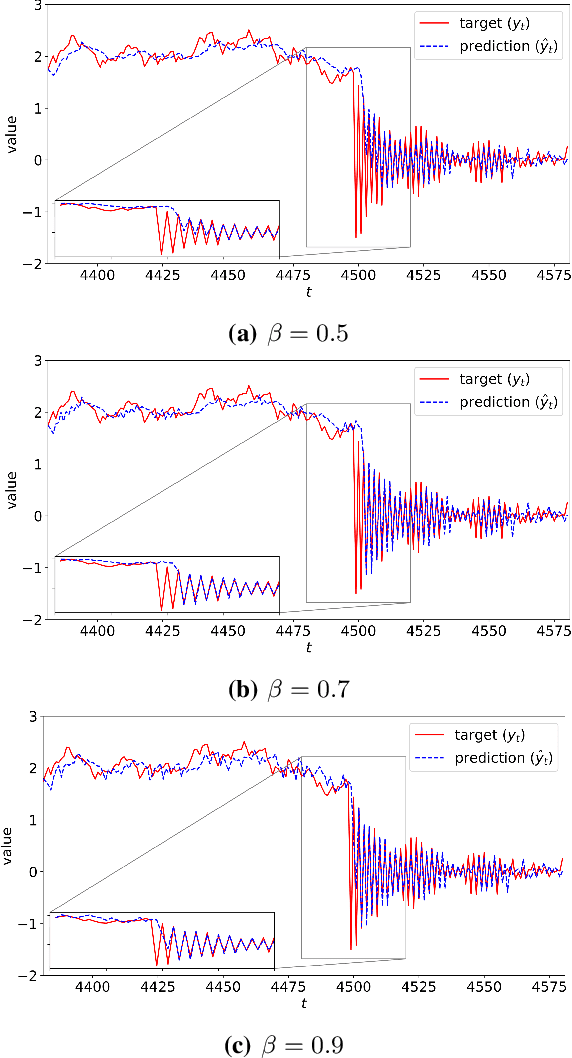

We investigate nonlinear regression for nonstationary sequential data. In most real-life applications such as business domains including finance, retail, energy and economy, timeseries data exhibits nonstationarity due to the temporally varying dynamics of the underlying system. We introduce a novel recurrent neural network (RNN) architecture, which adaptively switches between internal regimes in a Markovian way to model the nonstationary nature of the given data. Our model, Markovian RNN employs a hidden Markov model (HMM) for regime transitions, where each regime controls hidden state transitions of the recurrent cell independently. We jointly optimize the whole network in an end-to-end fashion. We demonstrate the significant performance gains compared to vanilla RNN and conventional methods such as Markov Switching ARIMA through an extensive set of experiments with synthetic and real-life datasets. We also interpret the inferred parameters and regime belief values to analyze the underlying dynamics of the given sequences.