Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeMarkov Decision Processes under Model Uncertainty

Paper and Code

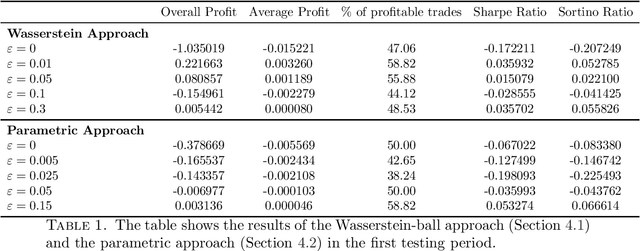

We introduce a general framework for Markov decision problems under model uncertainty in a discrete-time infinite horizon setting. By providing a dynamic programming principle we obtain a local-to-global paradigm, namely solving a local, i.e., a one time-step robust optimization problem leads to an optimizer of the global (i.e. infinite time-steps) robust stochastic optimal control problem, as well as to a corresponding worst-case measure. Moreover, we apply this framework to portfolio optimization involving data of the S&P 500. We present two different types of ambiguity sets; one is fully data-driven given by a Wasserstein-ball around the empirical measure, the second one is described by a parametric set of multivariate normal distributions, where the corresponding uncertainty sets of the parameters are estimated from the data. It turns out that in scenarios where the market is volatile or bearish, the optimal portfolio strategies from the corresponding robust optimization problem outperforms the ones without model uncertainty, showcasing the importance of taking model uncertainty into account.