Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeMachine Learning Classification of Price Extrema Based on Market Microstructure Features: A Case Study of S&P500 E-mini Futures

Paper and Code

Sep 21, 2020

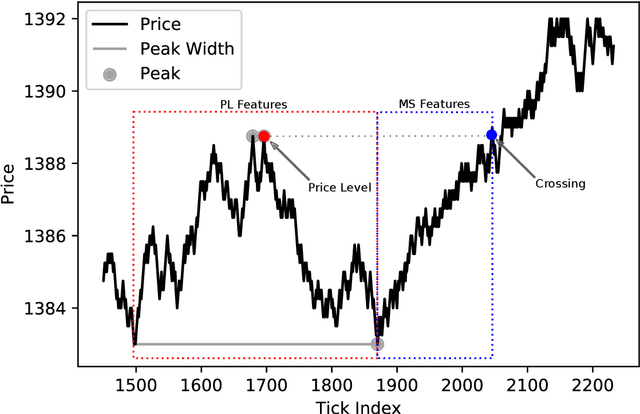

The study introduces an automated trading system for S\&P500 E-mini futures (ES) based on state-of-the-art machine learning. Concretely: we extract a set of scenarios from the tick market data to train the model and further use the predictions to model trading. We define the scenarios from the local extrema of the price action. Price extrema is a commonly traded pattern, however, to the best of our knowledge, there is no study presenting a pipeline for automated classification and profitability evaluation. Our study is filling this gap by presenting a broad evaluation of the approach showing the resulting average Sharpe ratio of 6.32. However, we do not take into account order execution queues, which of course affect the result in the live-trading setting. The obtained performance results give us confidence that this approach is worthwhile.