Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeIntra-day Equity Price Prediction using Deep Learning as a Measure of Market Efficiency

Paper and Code

Aug 22, 2019

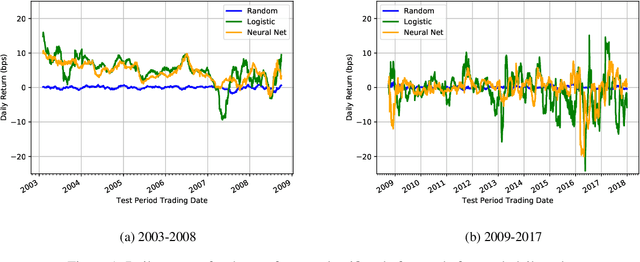

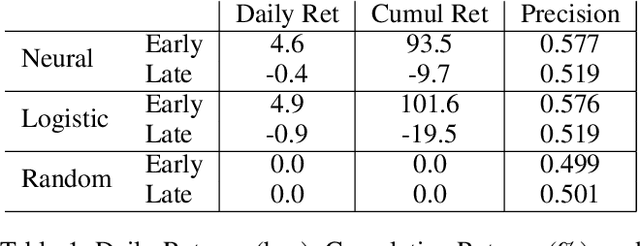

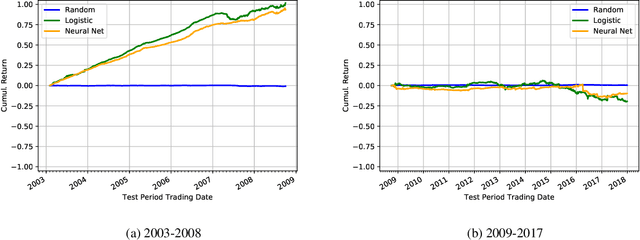

In finance, the weak form of the Efficient Market Hypothesis asserts that historic stock price and volume data cannot inform predictions of future prices. In this paper we show that, to the contrary, future intra-day stock prices could be predicted effectively until 2009. We demonstrate this using two different profitable machine learning-based trading strategies. However, the effectiveness of both approaches diminish over time, and neither of them are profitable after 2009. We present our implementation and results in detail for the period 2003-2017 and propose a novel idea: the use of such flexible machine learning methods as an objective measure of relative market efficiency. We conclude with a candidate explanation, comparing our returns over time with high-frequency trading volume, and suggest concrete steps for further investigation.