Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeHLOB -- Information Persistence and Structure in Limit Order Books

Paper and Code

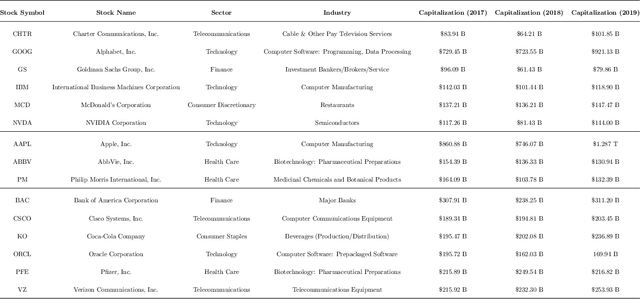

We introduce a novel large-scale deep learning model for Limit Order Book mid-price changes forecasting, and we name it `HLOB'. This architecture (i) exploits the information encoded by an Information Filtering Network, namely the Triangulated Maximally Filtered Graph, to unveil deeper and non-trivial dependency structures among volume levels; and (ii) guarantees deterministic design choices to handle the complexity of the underlying system by drawing inspiration from the groundbreaking class of Homological Convolutional Neural Networks. We test our model against 9 state-of-the-art deep learning alternatives on 3 real-world Limit Order Book datasets, each including 15 stocks traded on the NASDAQ exchange, and we systematically characterize the scenarios where HLOB outperforms state-of-the-art architectures. Our approach sheds new light on the spatial distribution of information in Limit Order Books and on its degradation over increasing prediction horizons, narrowing the gap between microstructural modeling and deep learning-based forecasting in high-frequency financial markets.