Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeHigh-dimensional variable selection

Paper and Code

Aug 20, 2009

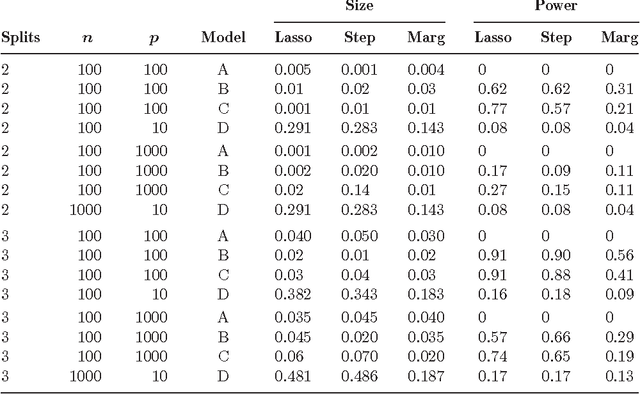

This paper explores the following question: what kind of statistical guarantees can be given when doing variable selection in high-dimensional models? In particular, we look at the error rates and power of some multi-stage regression methods. In the first stage we fit a set of candidate models. In the second stage we select one model by cross-validation. In the third stage we use hypothesis testing to eliminate some variables. We refer to the first two stages as "screening" and the last stage as "cleaning." We consider three screening methods: the lasso, marginal regression, and forward stepwise regression. Our method gives consistent variable selection under certain conditions.

* Annals of Statistics 2009, Vol. 37, No. 5A, 2178-2201 * Published in at http://dx.doi.org/10.1214/08-AOS646 the Annals of

Statistics (http://www.imstat.org/aos/) by the Institute of Mathematical

Statistics (http://www.imstat.org)

View paper on