Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeGradient Boosting Performs Low-Rank Gaussian Process Inference

Paper and Code

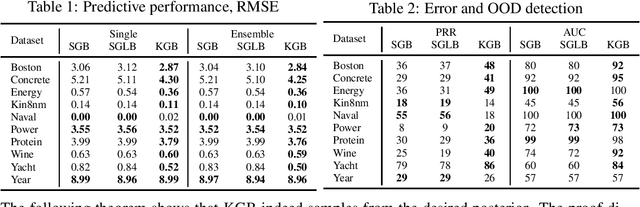

This paper shows that gradient boosting based on symmetric decision trees can be equivalently reformulated as a kernel method that converges to the solution of a certain Kernel Ridgeless Regression problem. Thus, for low-rank kernels, we obtain the convergence to a Gaussian Process' posterior mean, which, in turn, allows us to easily transform gradient boosting into a sampler from the posterior to provide better knowledge uncertainty estimates through Monte-Carlo estimation of the posterior variance. We show that the proposed sampler allows for better knowledge uncertainty estimates leading to improved out-of-domain detection.

View paper on

OpenReview

OpenReview