Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeGAS-Norm: Score-Driven Adaptive Normalization for Non-Stationary Time Series Forecasting in Deep Learning

Paper and Code

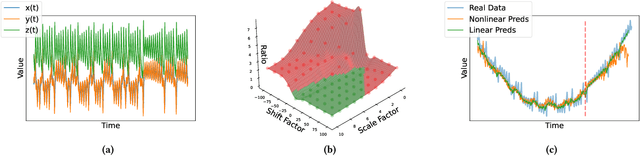

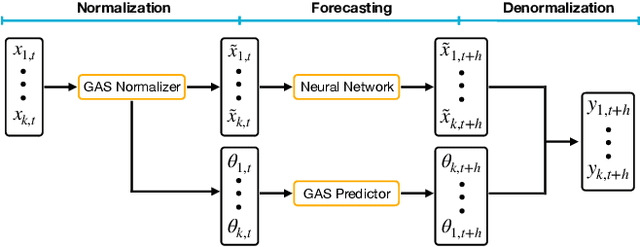

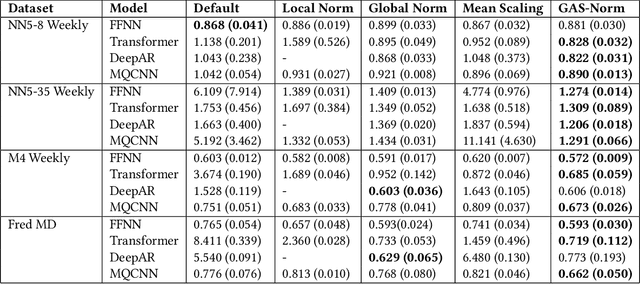

Despite their popularity, deep neural networks (DNNs) applied to time series forecasting often fail to beat simpler statistical models. One of the main causes of this suboptimal performance is the data non-stationarity present in many processes. In particular, changes in the mean and variance of the input data can disrupt the predictive capability of a DNN. In this paper, we first show how DNN forecasting models fail in simple non-stationary settings. We then introduce GAS-Norm, a novel methodology for adaptive time series normalization and forecasting based on the combination of a Generalized Autoregressive Score (GAS) model and a Deep Neural Network. The GAS approach encompasses a score-driven family of models that estimate the mean and variance at each new observation, providing updated statistics to normalize the input data of the deep model. The output of the DNN is eventually denormalized using the statistics forecasted by the GAS model, resulting in a hybrid approach that leverages the strengths of both statistical modeling and deep learning. The adaptive normalization improves the performance of the model in non-stationary settings. The proposed approach is model-agnostic and can be applied to any DNN forecasting model. To empirically validate our proposal, we first compare GAS-Norm with other state-of-the-art normalization methods. We then combine it with state-of-the-art DNN forecasting models and test them on real-world datasets from the Monash open-access forecasting repository. Results show that deep forecasting models improve their performance in 21 out of 25 settings when combined with GAS-Norm compared to other normalization methods.