Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeForex Trading Volatility Prediction using Neural Network Models

Paper and Code

Dec 03, 2021

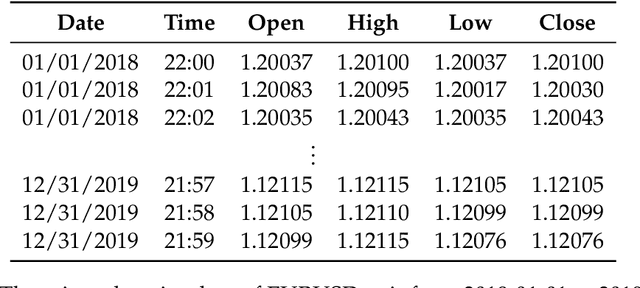

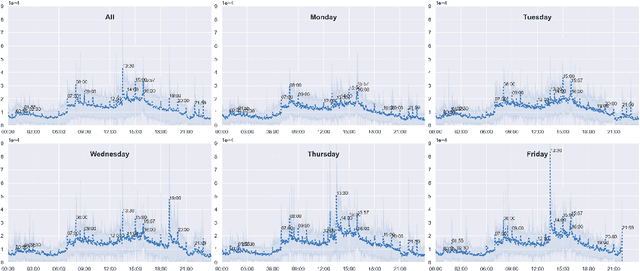

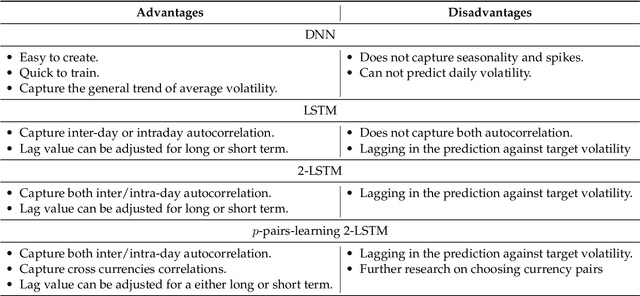

In this paper, we investigate the problem of predicting the future volatility of Forex currency pairs using the deep learning techniques. We show step-by-step how to construct the deep-learning network by the guidance of the empirical patterns of the intra-day volatility. The numerical results show that the multiscale Long Short-Term Memory (LSTM) model with the input of multi-currency pairs consistently achieves the state-of-the-art accuracy compared with both the conventional baselines, i.e. autoregressive and GARCH model, and the other deep learning models.

View paper on