Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeEstimating Time-Varying Graphical Models

Paper and Code

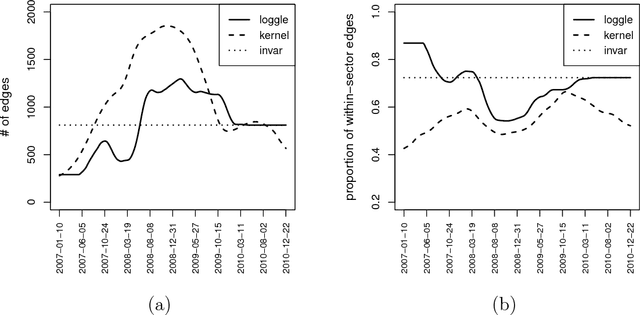

In this paper, we study time-varying graphical models based on data measured over a temporal grid. Such models are motivated by the needs to describe and understand evolving interacting relationships among a set of random variables in many real applications, for instance the study of how stocks interact with each other and how such interactions change over time. We propose a new model, LOcal Group Graphical Lasso Estimation (loggle), under the assumption that the graph topology changes gradually over time. Specifically, loggle uses a novel local group-lasso type penalty to efficiently incorporate information from neighboring time points and to impose structural smoothness of the graphs. We implement an ADMM based algorithm to fit the loggle model. This algorithm utilizes blockwise fast computation and pseudo-likelihood approximation to improve computational efficiency. An R package loggle has also been developed. We evaluate the performance of loggle by simulation experiments. We also apply loggle to S&P 500 stock price data and demonstrate that loggle is able to reveal the interacting relationships among stocks and among industrial sectors in a time period that covers the recent global financial crisis.