Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeEmpirical Risk Minimization under Random Censorship: Theory and Practice

Paper and Code

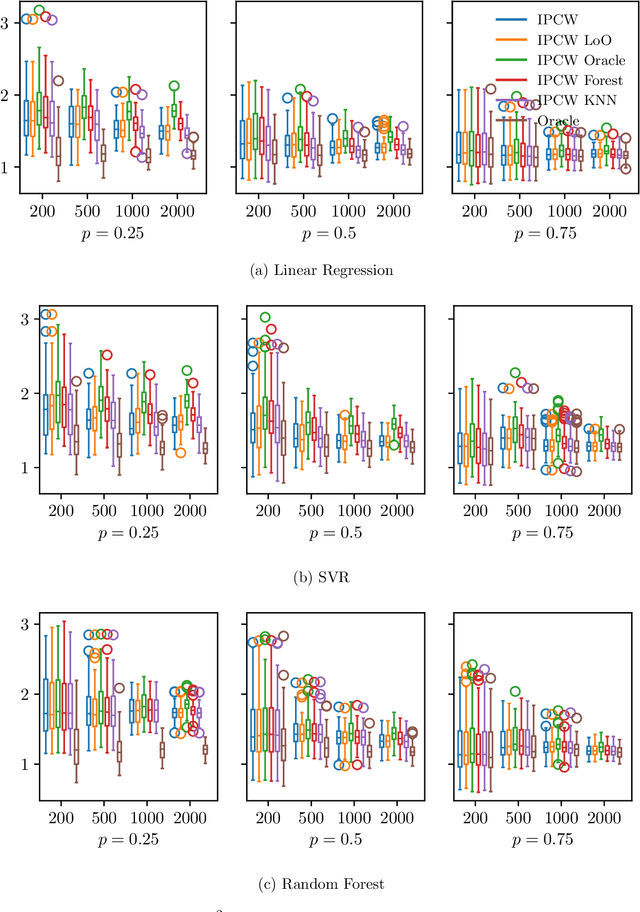

We consider the classic supervised learning problem, where a continuous non-negative random label $Y$ (i.e. a random duration) is to be predicted based upon observing a random vector $X$ valued in $\mathbb{R}^d$ with $d\geq 1$ by means of a regression rule with minimum least square error. In various applications, ranging from industrial quality control to public health through credit risk analysis for instance, training observations can be right censored, meaning that, rather than on independent copies of $(X,Y)$, statistical learning relies on a collection of $n\geq 1$ independent realizations of the triplet $(X, \; \min\{Y,\; C\},\; \delta)$, where $C$ is a nonnegative r.v. with unknown distribution, modeling censorship and $\delta=\mathbb{I}\{Y\leq C\}$ indicates whether the duration is right censored or not. As ignoring censorship in the risk computation may clearly lead to a severe underestimation of the target duration and jeopardize prediction, we propose to consider a plug-in estimate of the true risk based on a Kaplan-Meier estimator of the conditional survival function of the censorship $C$ given $X$, referred to as Kaplan-Meier risk, in order to perform empirical risk minimization. It is established, under mild conditions, that the learning rate of minimizers of this biased/weighted empirical risk functional is of order $O_{\mathbb{P}}(\sqrt{\log(n)/n})$ when ignoring model bias issues inherent to plug-in estimation, as can be attained in absence of censorship. Beyond theoretical results, numerical experiments are presented in order to illustrate the relevance of the approach developed.