Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeEfficient Black-Box Importance Sampling for VaR and CVaR Estimation

Paper and Code

Jun 16, 2021

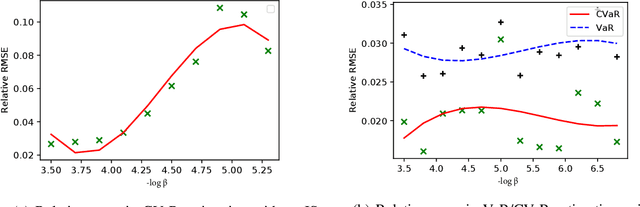

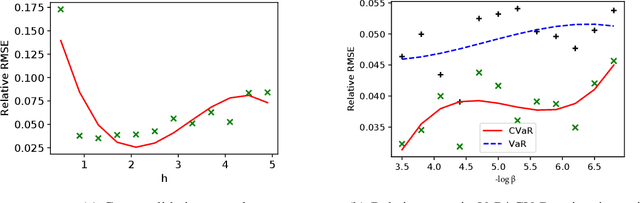

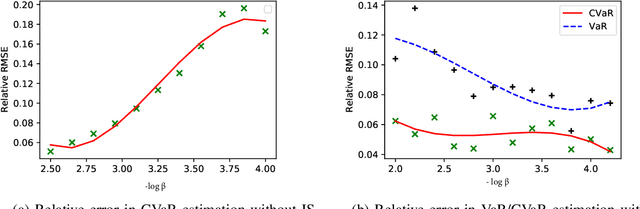

This paper considers Importance Sampling (IS) for the estimation of tail risks of a loss defined in terms of a sophisticated object such as a machine learning feature map or a mixed integer linear optimisation formulation. Assuming only black-box access to the loss and the distribution of the underlying random vector, the paper presents an efficient IS algorithm for estimating the Value at Risk and Conditional Value at Risk. The key challenge in any IS procedure, namely, identifying an appropriate change-of-measure, is automated with a self-structuring IS transformation that learns and replicates the concentration properties of the conditional excess from less rare samples. The resulting estimators enjoy asymptotically optimal variance reduction when viewed in the logarithmic scale. Simulation experiments highlight the efficacy and practicality of the proposed scheme