Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeDeepVARMA: A Hybrid Deep Learning and VARMA Model for Chemical Industry Index Forecasting

Paper and Code

Apr 26, 2024

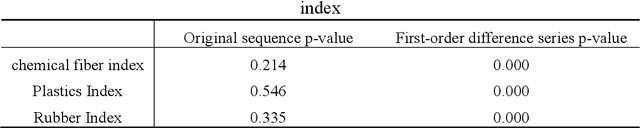

Since the chemical industry index is one of the important indicators to measure the development of the chemical industry, forecasting it is critical for understanding the economic situation and trends of the industry. Taking the multivariable nonstationary series-synthetic material index as the main research object, this paper proposes a new prediction model: DeepVARMA, and its variants Deep-VARMA-re and DeepVARMA-en, which combine LSTM and VARMAX models. The new model firstly uses the deep learning model such as the LSTM remove the trends of the target time series and also learn the representation of endogenous variables, and then uses the VARMAX model to predict the detrended target time series with the embeddings of endogenous variables, and finally combines the trend learned by the LSTM and dependency learned by the VARMAX model to obtain the final predictive values. The experimental results show that (1) the new model achieves the best prediction accuracy by combining the LSTM encoding of the exogenous variables and the VARMAX model. (2) In multivariate non-stationary series prediction, DeepVARMA uses a phased processing strategy to show higher adaptability and accuracy compared to the traditional VARMA model as well as the machine learning models LSTM, RF and XGBoost. (3) Compared with smooth sequence prediction, the traditional VARMA and VARMAX models fluctuate more in predicting non-smooth sequences, while DeepVARMA shows more flexibility and robustness. This study provides more accurate tools and methods for future development and scientific decision-making in the chemical industry.