Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeConvergence Analysis of Machine Learning Algorithms for the Numerical Solution of Mean Field Control and Games: II -- The Finite Horizon Case

Paper and Code

Aug 05, 2019

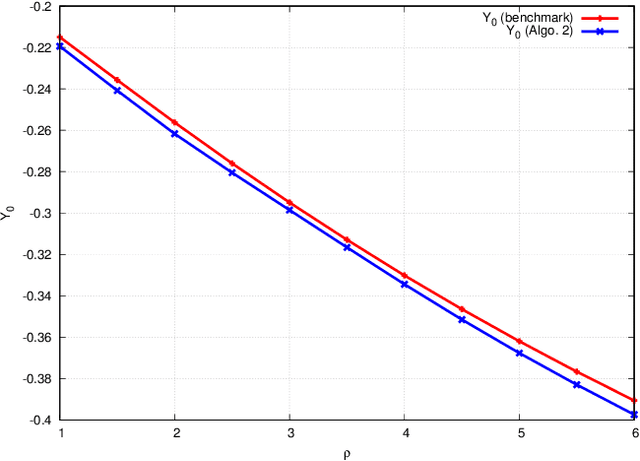

We propose two numerical methods for the optimal control of McKean-Vlasov dynamics in finite time horizon. Both methods are based on the introduction of a suitable loss function defined over the parameters of a neural network. This allows the use of machine learning tools, and efficient implementations of stochastic gradient descent in order to perform the optimization. In the first method, the loss function stems directly from the optimal control problem. We analyze the approximation and the estimation errors. The second method tackles a generic forward-backward stochastic differential equation system (FBSDE) of McKean-Vlasov type, and relies on suitable reformulation as a mean field control problem. To provide a guarantee on how our numerical schemes approximate the solution of the original mean field control problem, we introduce a new optimization problem, directly amenable to numerical computation, and for which we rigorously provide an error rate. Several numerical examples are provided. Both methods can easily be applied to problems with common noise, which is not the case with the existing technology. Furthermore, although the first approach is designed for mean field control problems, the second is more general and can also be applied to the FBSDE arising in the theory of mean field games.