Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeConstructing Financial Sentimental Factors in Chinese Market Using Natural Language Processing

Paper and Code

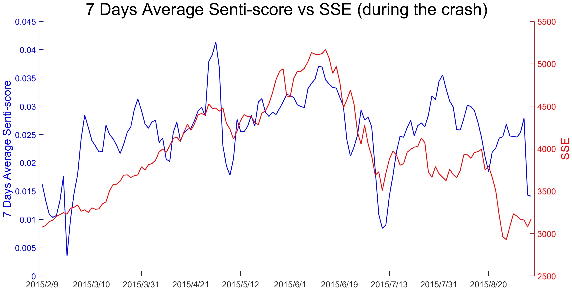

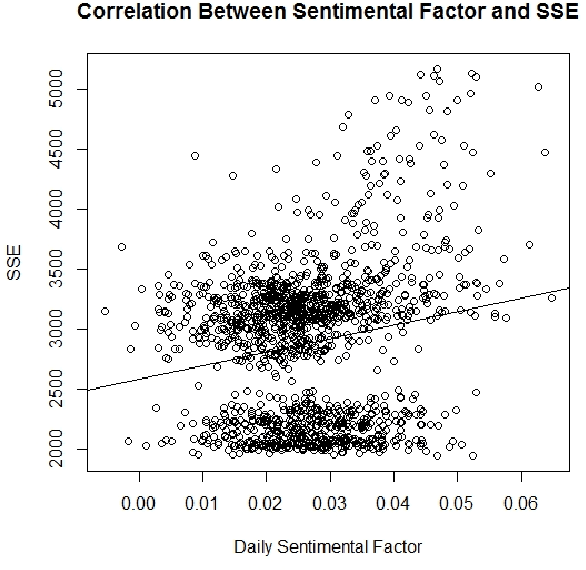

In this paper, we design an integrated algorithm to evaluate the sentiment of Chinese market. Firstly, with the help of the web browser automation, we crawl a lot of news and comments from several influential financial websites automatically. Secondly, we use techniques of Natural Language Processing(NLP) under Chinese context, including tokenization, Word2vec word embedding and semantic database WordNet, to compute Senti-scores of these news and comments, and then construct the sentimental factor. Here, we build a finance-specific sentimental lexicon so that the sentimental factor can reflect the sentiment of financial market but not the general sentiments as happiness, sadness, etc. Thirdly, we also implement an adjustment of the standard sentimental factor. Our experimental performance shows that there is a significant correlation between our standard sentimental factor and the Chinese market, and the adjusted factor is even more informative, having a stronger correlation with the Chinese market. Therefore, our sentimental factors can be important references when making investment decisions. Especially during the Chinese market crash in 2015, the Pearson correlation coefficient of adjusted sentimental factor with SSE is 0.5844, which suggests that our model can provide a solid guidance, especially in the special period when the market is influenced greatly by public sentiment.